WHY SAVING FOR RETIREMENT IS SO HARD

We want to be able to retire with enough money to support ourselves in reasonable comfort. That means saving relentlessly over the years. It also means anticipating the financial threats that face us now and in the future. We must correctly identify our enemies.

Our enemies are those whose goal is to put our money into their pockets. They include fraudsters like Bernie Madoff, stock bond and cryptocurrency “pumpers-and-dumpers,” account hackers, phone and internet scammers. However, the most dangerous enemy is our own governing elite. Throughout history, it has been their goal to extract the maximum amount of wealth from us to empower and enrich themselves.

In ancient Egypt the pharaohs possessed vast wealth while everyone else labored dawn to dusk building their pyramids. In the Middle Ages, European kings drained wealth from their subjects to fight wars, build palaces and live large off the sweat of the brow of the people who died in the wars, never saw the inside of the palaces, and lived hand-to-mouth in desperate conditions.

There are still people actively working behind the scenes to frustrate our efforts to save and grow our money. The US Federal Reserve Bank has two mandates: maintain price stability and achieve full employment. While these are noble sounding goals that should inure to our collective benefit, the fact is that for decades the Fed has been acting in ways designed to enrich the few while punishing the many who are trying to salt away enough to support themselves in retirement.

Years of Fed-imposed low interest rates have goosed the stock market and inflated asset bubbles. Low rates make it easy for the well connected to borrow cheaply and invest on margin. This enriches the 10% who own the lion’s share of stocks and other investable assets. Low rates also allow corporations to borrow cheaply to buy back their shares thereby enriching corporate officers through their stock options.

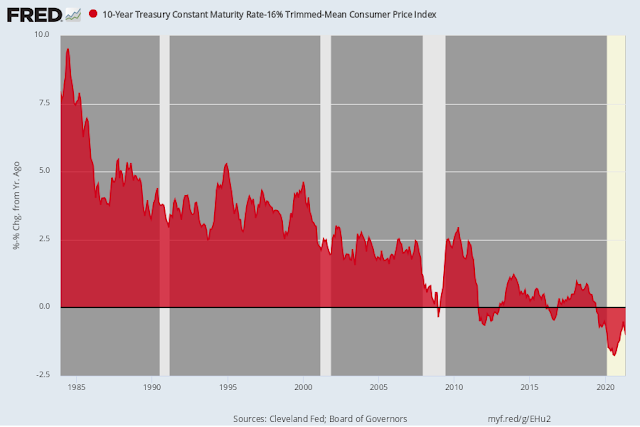

Most workers own no stocks. They typically save for retirement by putting money into bank certificates of deposit. For decades the Fed has been artificially forcing interest rates down. As a result, people with savings are losing money every month. Banks pay less than 1% interest on savings. However, price inflation is now 5% according to the “official” consumer price index and 8-12% if calculated without accounting gimmicks designed to hide the real rate of price inflation. As a result, savers are being relentlessly robbed. Here is the 10-year Treasury interest rate less the “official” inflation rate. The result is negative returns. You are losing money. However, the reality is much worse.

If your bank secretly skimmed 5% of your savings annually, you would be outraged. But the Fed is taking that much and more each year through the process of devaluing the dollars in your account. What is insidious about it is that most people have no clue they are being victimized and even if they suspect it, they have no understanding of who is responsible for it.

Politicians learned long ago that there are limits to the amount of direct taxation that people will endure. But the sums raised by direct taxation are never enough for the political insiders who have insatiable demands for more wealth and power. Thus, a means had to be devised to extract more wealth from the “proles” in a surreptitious way. Devaluation of the currency is their answer. As the Fed prints trillions of new dollars, those dollars compete for the existing supply of goods, services and assets. This rapid inflation (growth) of the money supply inevitably results in higher prices.

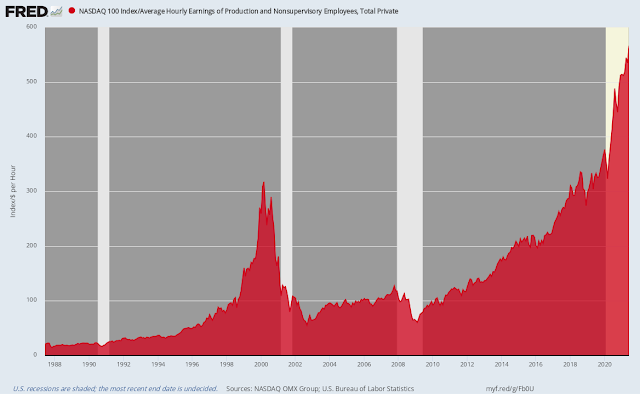

Higher prices mean that the value of your income and savings is continually diminished. Most people sell their time to their employers in exchange for a salary. Even if their salary increases slowly over time, the value of their time is being constantly reduced. They get poorer without understanding why. Those living on a fixed income, such as social security or a pension, find it ever harder to make ends meet even though their income in dollars remains stable. This chart shows how many hours the average wage earner has had to work over the years to buy the NASDAQ 100.

The Fed’s 2% Inflation Target

Chairman Powell at the Fed has told us repeatedly that he is aiming for 2% price inflation and will let it run higher to make up for periods when it has been below that threshold. Two percent inflation does not sound terrible but it has dramatic consequences for you. Suppose you work hard and are able to salt away $1M by the time you are 45. Your retirement plan is to withdraw 4% a year ($40,000) to supplement your social security ($30,000) to be able to live comfortably on the $70,000. But with 2% price inflation, by the time you are 65, your $1M will have the purchasing power of just $667,608. You will have lost one-third of your savings. If you take out $40,000 a year you will almost certainly outlive your savings. If price inflation is higher – say 4% - your situation would become desperate. You will have lost two-thirds of your savings. You will have the purchasing power of just $335,216 at 65 and that would continue to shrink throughout your retirement. Thus, the Fed’s 2% inflation “goal” is going to be an unmitigated disaster for us.

Price inflation is already far higher than reported in the media and by Chairman Powell. John Williams of ShadowStats.com continues to calculate price inflation as the government did before the Clinton presidency. That is, he ignores the “hedonic adjustments” that intentionally distort the prices faced by real people in the real economy and he includes food and energy that people use every day but are ignored by the Fed with the excuse that they are “volatile.” They may be volatile but they are no less essential. Will you stop heating your home in the winter and eating when prices become volatile? Food and energy cannot be ignored if one is honest about reporting price increases.

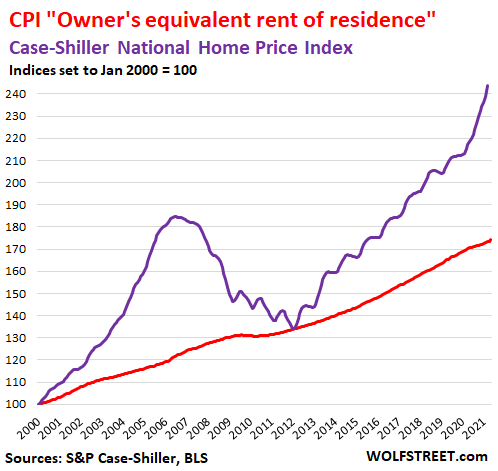

Another way the government falsifies price inflation is by ignoring actual housing expenses by substituting its theoretical construct of “owner’s equivalent rent.” Housing is most people’s biggest monthly expense. Real housing costs (blue line) are much higher than reported by the government.

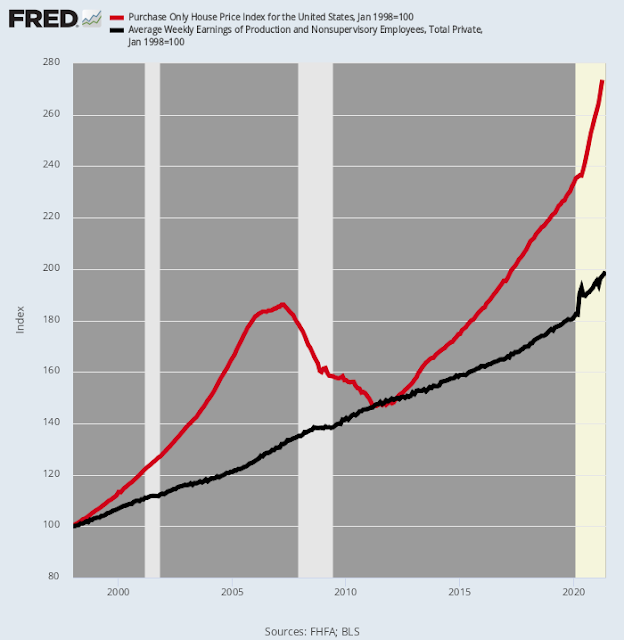

As the Fed fuels yet another housing bubble with artificially low interest rates, the lower and middle classes are being priced out of the market. This chart shows the yawning divide between average wages (black line) and rising housing prices (red line).

Politicians always encourage us to blame “greedy businesses” for rising prices. However businesses have no option but to increase prices as their input costs (labor and materials) increase due to the inflation of the money supply by the government. If they did not raise prices, they would soon go out of business. As economist Milton Friedman famously observed, “Inflation is always and everywhere a monetary phenomenon in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output.”

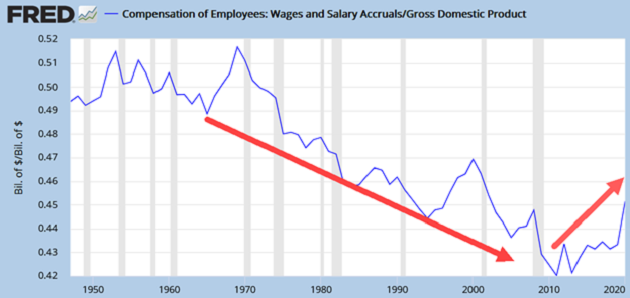

We can observe this price-inflation/dollar-devaluation in different ways. The chart on the next page shows the long-term decline in real wages and salaries relative to GDP.

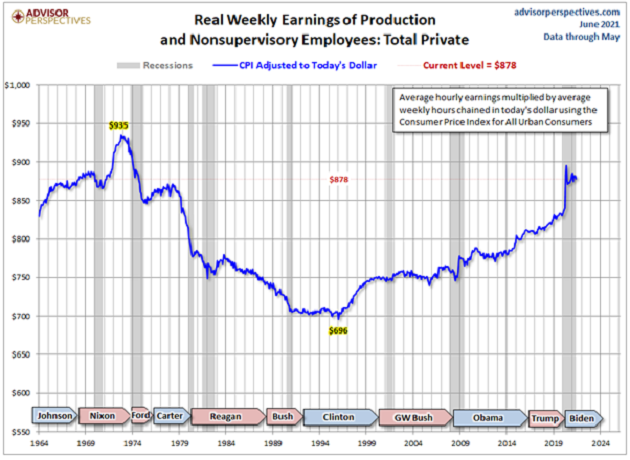

Another way to visualize this is to compare real wages (net of price inflation) to earlier years. We see below that workers today are making less money in real terms than during the Nixon presidency.

US and EU politicians are hell-bent on running large deficits to fund their vastly expanded spending, the effect of which will be to further diminish the value of workers’ wages and salaries. While there is much talk about “taxing the rich” to pay for it, it is always the lower and middle classes who pay the dearest price for rising prices. Vast numbers of people are finding it ever harder to maintain their standard of living. The next chart shows why.

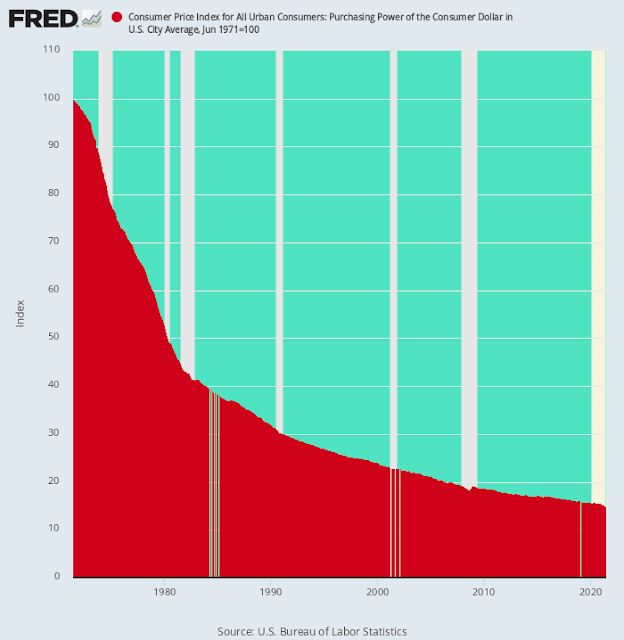

The US dollar today has just fifteen cents in purchasing power compared to the 1971 dollar. That was when the dollar became untethered to the price of gold. That untethering has allowed the government to print trillions of dollars that inexorably lead to higher prices.

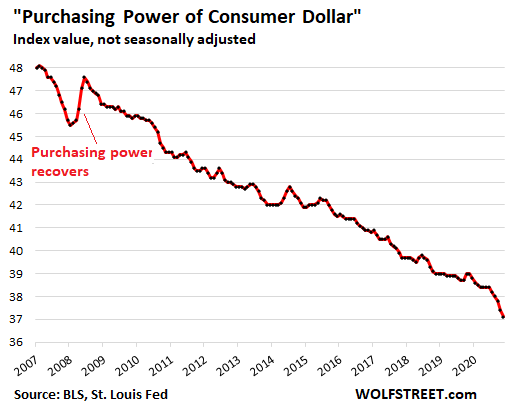

This next chart shows the loss of the dollar’s purchasing power over just the last fourteen years.

If you look farther back in time to the beginning of the Federal Reserve Bank in 1913, you discover that the dollar has lost more than 97% of its purchasing power. This devaluation will continue as the Fed continues to print dollars to close the yawning gap between government revenues and expenses ($3T this year in the US).

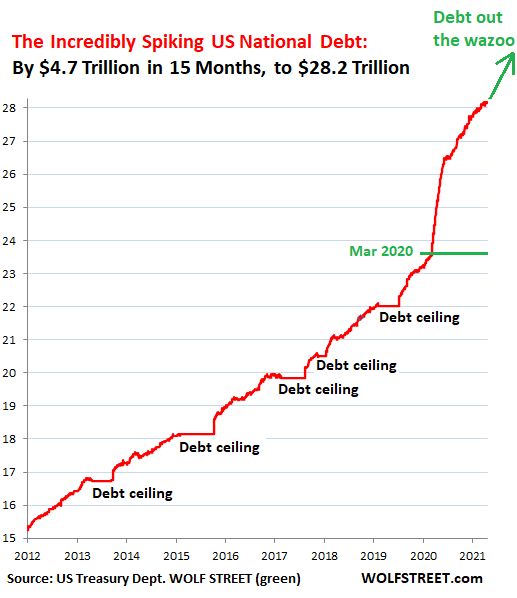

Soaring Debt Levels

The US national debt will soon reach $30 trillion. It was $20T when Trump came to office. Think about that. The national debt has increased 50% in just five years. And President Biden has another $5T in spending on his wish list.

The Fed wants to generate price inflation to address this surging debt. Why? Because a negative 3% real interest rate (e.g., interest rate of 1% coupled with price inflation at 4% = -3% real rate) reduces the real value of that debt by 46% over 20 years. At negative 5%, the real value of the debt is reduced by 64%. Through this means the US government will stiff its creditors.

Sadly, the “official” US national debt is just the tip of the debt iceberg. The real kicker comes in the form of “unfunded liabilities.” These are future expenses that Uncle Sam has committed to paying, such as $21.2 trillion for Social Security and $32.9 trillion for Medicare. Add up all such obligations and it is estimated that the US’s liabilities exceed $140 trillion. Obviously, the US in incapable of paying that in honest money. What it is incapable of doing, it will not do. But the government will not default on these dollar obligations. It will just print more money to pay them. That means we will continue to suffer a “soft default” with dollar and Treasury bond holders paying the direct cost and everyone paying the indirect cost of devaluation.

Decades of Fed money printing has fueled bubbles in every asset classes. While this sounds like good news for investors, it comes with a sting. David Stockman sums it up: “Well-nigh all of today’s economic ills arise from it. These include slowing growth, hollowed-out industry, stagnant wages, rising wealth maldistribution, runaway government debt, massive speculation and financial bubbles, a nation of indentured debt slaves, and now surging prices for goods and services, too.” Those are very high prices to pay. Who pays them? The 1%? The 10%? No, they have benefited massively from asset price inflation. It is always the lower and middle classes that disproportionately suffer these consequences.

The Fed argues that by falsifying interest rates for twenty years and vastly expanding the money supply, it is on the verge of creating the perfect economy with full employment and 2% inflation. It repeatedly assures us that recent price inflation exceeding 5% is “transitory” and will soon level off near its 2% goal. Few people share the Fed’s confidence. Mohamed El-Erian, economist at Allianz and frequent Financial Times editorial contributor sees growing evidence that the Fed is dangerously behind the curve. “I have concerns about the inflation story. Every day I see evidence of inflation not being transitory, and I have concern that the Fed is falling behind and that it may have to play catch-up, and history makes you very uncomfortable if you end up in a world in which the Fed has to play catch-up.” He means that when the Fed is forced to abruptly increase interest rates to fight surging inflation it will trigger a market collapse and deep recession.

David Stockman has long argued that the Fed’s massive intrusion in the markets “obliterates honest price discovery, thereby systematically and deeply falsifying the price of money, debt, equities and other derivatives and tradable assets such as cryptos and NFTs, which get swept up in the resulting speculative bubbles.” Falsified interest rates and a rapidly growing money supply cause investors to make bad decisions they will pay for dearly in the future. The TV show Frontline recently had a report on what the Fed has been doing and the risks associated with it. You can view it at https://www.youtube.com/watch?v=9RbL8lTsITY

Charles Hugh Smith sums up our fraught situation:

Are you prepared to be punched in the mouth? Van Hoisington explains why today’s stratospheric debt levels come with a built-in upper cut.It always ends the same way. One of the most under-appreciated investment insights is courtesy of Mike Tyson: "Everybody has a plan until they get punched in the mouth." In other words, the vast majority of punters are convinced they will never suffer the indignity of getting punched in the mouth by a market crash. What makes this confidence so interesting is that massively distorted markets always end the same way: crisis, crash and collapse.The core dynamic here is: distorted markets provide false feedback and misleading information which then lead to participants making catastrophically misguided decisions. The surprise comes from the falsity of the feedback, as those who are distorting markets want punters to believe "the market" is functioning transparently. If you're manipulating the market, the last thing you want is for the unwary marks to discover that the market is generating false signals and misleading information on risk, as knowing the market is being distorted would alert them to the extraordinary risks intrinsic to heavily distorted markets. Another source of risk in distorted markets is the illusion of liquidity: On top of all these grossly misleading distortions, punters have been encouraged to believe in the ultimate distortion: the Federal Reserve will never let markets decline again, ever. This is the perfection of moral hazard: risk has been disconnected from consequence. Risk cannot be extinguished; it can only be transferred. By distorting markets to create an illusion of low-risk stability, the Federal Reserve has transferred this fatal supernova of risk to the entire financial system.

Today, the best evidence suggests the following: (1) monetary and fiscal actions are largely impotent in stimulating economic activity due to the massive debt overhang in the U.S. and most major foreign economic powers; (2) while taking on more debt does produce a fleeting benefit for economic growth, such actions embroil the economies deeper in a debt trap; (3) central bank tools have the capability of restraining economic activity, as was illustrated by tightening actions from 2016 to 2018; (4) fiscal restraint would temporarily diminish economic growth, but if it could be sustained, the debt overhang could be worked off and in time the economy would recover. However, in a democracy it is highly unlikely that a program of fiscal austerity would even be proposed and if taken, surely not sustained. At the first sight of transitory weakness, the body politic would demand an easing of the restraint. However, modern democracies demand action even if the solutions only make matters worse. The main obstacle to a return to sustained growth in the standard of living, extreme over-indebtedness, was dramatically worsened by the multiple rounds of fiscal stimulus, which have caused the temporary improvement in economic growth and inflation in the second quarter. No pathway out of this trap exists as long as the overreliance on debt remains the only tool of monetary and fiscal policy. The situation is no different in Japan and Europe. (Emphasis added).

The Growing Wealth Disparity

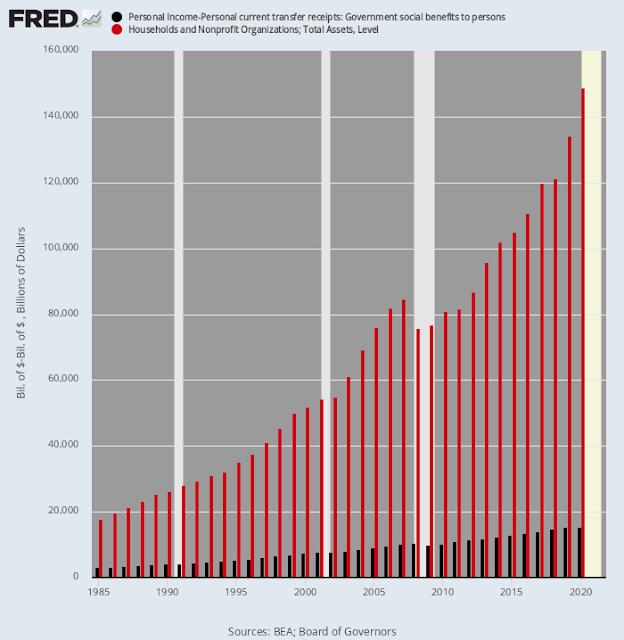

Here we see the growth in government benefits (black bars) and the growth of the value of assets (red bars). Those who own assets have fared vastly better from the Fed’s policies than those who receive benefits.

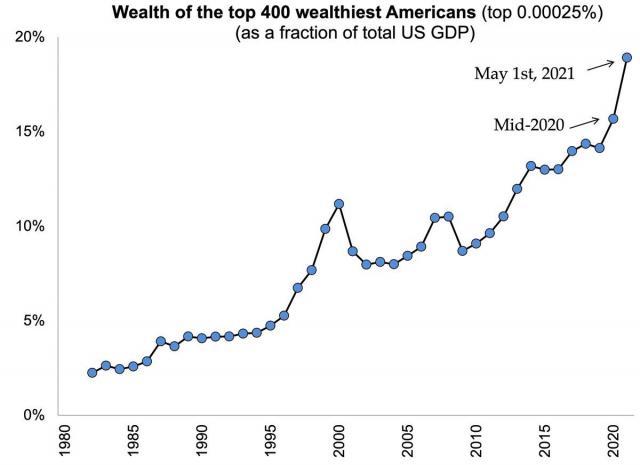

In 1980 the wealth of the richest 400 Americans was equal to 2.5% of US GDP. They now hold wealth equal to 20% of the US GDP.

History teaches that excessive financial inequality inevitably leads to social instability. That message is lost on politicians. It is their belief that if they dangle a few social welfare benefits in front of the masses, that will keep them quiet while the insiders continue to line their own pockets.

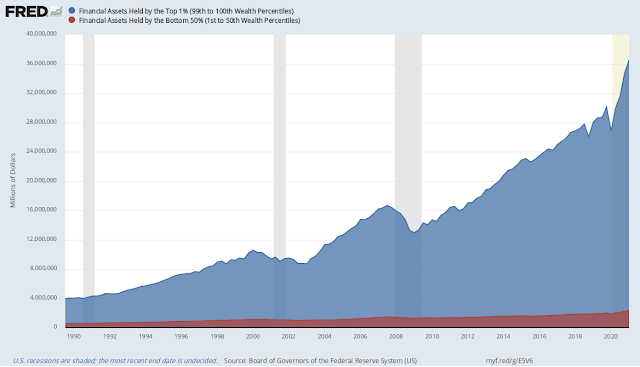

Another view of this disparity is to compare the wealth of the top 1% (blue) to the wealth held by the bottom 50% (red). The Fed’s policies have been directly responsible for this outcome.

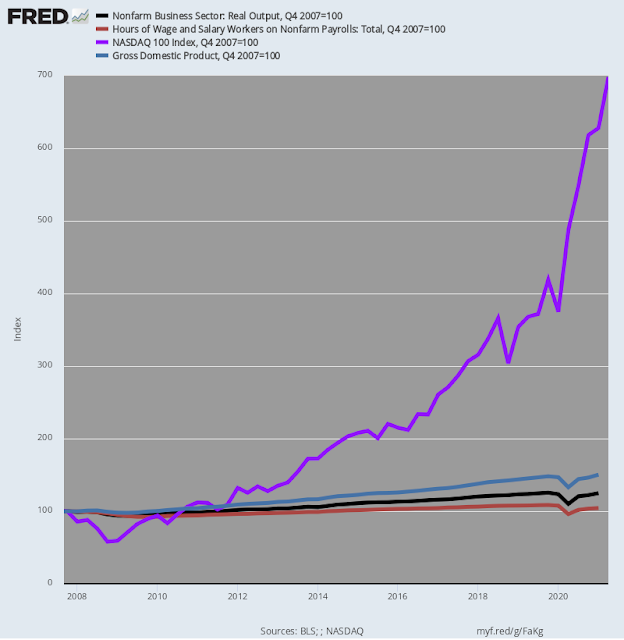

The chart on the next page shows the divergence between the growth of the US economy (all of us) and the growth of asset prices (few of us). The black line is non-farm real output, the red line is non-farm hours and wages, the green line is growth in GDP. The blue line soaring up and to the right is the NASDAQ 100 Index. There is no longer any correlation between the real economy and the market. Pundits justify this with the explanation that the markets are “forward looking” while economic data are “backward looking.” While true, it is impossible to correlate the “irrational exuberance” of the markets at current levels with reasonable projections of future revenue growth. Markets overreach and then inevitably “correct.” Economists call this process “reverting to the mean.” Investors call it a “market debacle.”

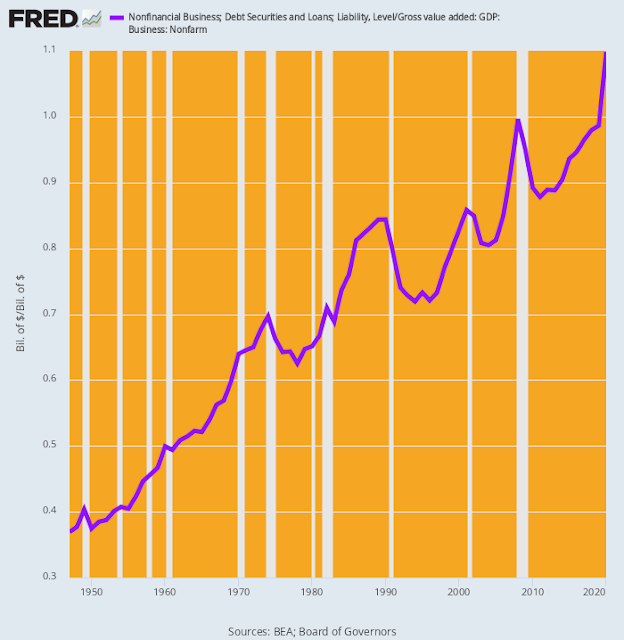

The Fed’s artificial low interest rates have encouraged non-financial US companies to gorge on new debt - to the tune of $11.2T. That is equal to one-half the US national output. Some companies are sitting on their cash waiting to see what happens next. Others have used it to buy back their stock in order to goose their executive’s bonuses or engage in M&A activity that rarely produces long term growth. Precious little of it has been used for capital expenditures to improve productivity, meaning there will be no enhanced revenue stream to service the growing debt.

The stampede into junk bonds in a desperate search for yield has driven up the price of low-grade, high-risk products to the point that Greece, the basket case of the EU, was recently able to sell bonds bearing a real negative return.

Another disturbing fact that the main stream media studiously ignore is that 25% of the US Russell 3000 businesses are “zombies,” meaning they cannot even pay the interest on their existing debt from revenues, much less repay the principle. It does not take a rocket scientist to understand that even a small rise in interest rates or an unexpected loss of liquidity is all it will take to sink their ships (think 2008 – on steroids) and again threaten the major banks. This chart shows the soaring growth of non-financial business debt.

The Pandemic Bailouts

At least Americans can take solace in the fact that the hundreds of billions of dollars distributed during the Covid shut-down went to hard working, down-on-their-luck people who were forced into unemployment. If only. Axios reports that unemployment fraud rose heavily during the pandemic with thieves stealing as much as half of the benefits dished out over the last year. Blake Hall of fraud prevention service ID.me says that the US lost $400B to fraudulent claims with as much as 70% of the stolen money leaving the country to criminals in China, Russia and Nigeria.

While tens of millions of US workers were struggling with job losses, no tears were shed for corporate executives. Eight CEO’s received pay packages worth at least $100M in 2020. But they were pikers. Alex Karp of Palantir “earned” $1.1 billion, Tony Xu of DoorDash banked $414M and Eric Wu of Opendoor walked away with $370M while the formerly prosperous US middle class were becoming today’s debt serfs. In the last sixty years total household debt has risen 84x, increasing from $194B in 1959 to $16.328T in 2020. Wages and salaries have risen in “nominal” terms (ignoring inflation) by only 36x. However, in real terms, wage gains were non-existent. It is no wonder that so many people are struggling to keep their noses above water.

A Final Word

There has been a very troubling change in our local news and there are similar reports coming out of most major US cities. It became most obvious following the BLM marches-cum-riots where thousands of “protesters” flooded Michigan Avenue, looted stores, lit cars on fire and terrorized local residents. Law enforcement authorities were unprepared, underequipped and outmanned. Crime is surging and the police are clearly losing control of the situation. Here are some headlines from the Chicago Tribune:

- 3 dead, 34 wounded in Memorial Day weekend shootings

- Woman, 86, shot while watering grass

- Carjacker shoots man in head changing tire

- 8 dead, 38 hurt in weekend shootings

- 77 shot in weekend violence with 17 dead

- Teen shot while walking dog

- 12 fatalities among 73 shot over weekend

- 15 year old charged with stabbing robbery victim on CTA train

- Teen charged in 3 car jackings

- 8 shot at weekend grad party

- Girl 15 shot on Lake Shore Drive

- Over 50 people shot over the weekend, 5 fatally

- At least 108 people shot – 17 fatally during July 4th holiday weekend

Homicides have risen 24% in a sample of 32 US cities in the first quarter of 2021. Much of the rise can be attributed to short-sighted politics. For example, Portland Oregon decided to “defund” its police department by $15M following the BLM riots including its 38-person gun violence team. Homicide rates subsequently soared and the police will now form a new team to combat the surge.

Big cities have always had to deal with elevated levels of crime but the breadth and depth of it is shocking. In San Francisco, Walgreens chose to close seventeen stores that were being looted daily after politicians raised the limit for misdemeanor theft to $950. “Shoppers” now arrive with duffle bags and walk out with merchandise just below that limit knowing they will not be arrested or prosecuted.

When government fails to enforce the law and protect its citizens from predators, it fails its most essential function. Absent a prompt reversal of this trend, cities will continue to shed population and tax revenue and continue their financial death spiral. It is evident that the mayors of these cities are clueless about what to do. This all but ensures that things will get worse before they get better.

© All rights reserved 2021

If you find this material interesting feel free to sign up to have it delivered directly to you by going to WorldViewInvesting.com, click on the top left corner icon and select the “Subscribe” button. We will not share your email with anyone. If you are not receiving issues, please check your spam/junk folder and then “whitelist” us.

Important Message: The foregoing is not a recommendation to purchase or sell any security or asset, or to employ any particular investment strategy. Only you, in consultation with your trusted investment advisor, can select the strategy that meets your unique circumstances, investment objectives and risk tolerance.