WHERE DO THE MONSTERS LURK?

The Fed assures us that the major US banks are in good health and have passed rigorous stress tests that ensure taxpayers will not have to bail them out yet again at the next financial crisis. The banks’ health is critical to the US economy. When they are stressed their ability to lend to corporations and individuals is severely restricted and the economy quickly suffers.

What brought numerous banks to their knees in 2008 were their risky bets on the US housing market. They were lending to virtually anyone who could fog a mirror based on the flawed premise that housing prices never go down and therefore their mortgages were fully collateralized. Bond rating companies added to the frenzy by giving mortgage-backed securities “AAA” ratings, at the same time that bankers who were shopping them to their customers were internally referring to them as “crap.” After housing prices reached absurd levels there were not enough new buyers to keep bidding prices up. Mortgage repayment defaults grew and home prices began to fall – slowly at first and then rapidly. Both banks and investors were left holding a bag of increasingly worthless mortgages.

The banks thought they had been clever by laying-off much of their mortgage loan risk on other banks and insurers through insurance-like derivative instruments. These derivatives were nothing more than a daisy chain of promises. All it took was for one large derivative obligor to default and losses quickly flowed backward through the system. That is why the Fed had to bail out not just insolvent banks but also entities like AIG Insurance Company that had underwritten many of the derivative contracts but had woefully insufficient reserves to make good on the growing losses.

Pam and Russ Martens have written extensively about the 2008 sub-prime mortgage crisis. Here they recount why the danger not only persists today – but, is vastly bigger:

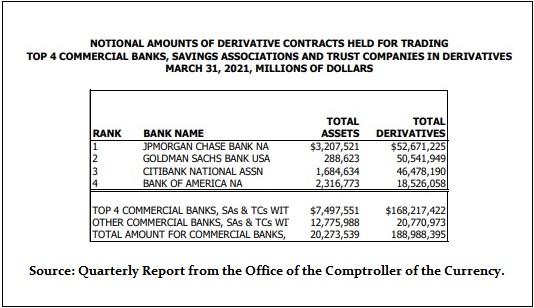

Risky derivative bets made by the mega banks on Wall Street, offloaded onto inadequately capitalized counterparties, were at the core of the collapse of the U.S. financial system in 2008. That collapse left millions of Americans without jobs, which led to millions of families and traumatized children losing their homes to foreclosure. The bank bosses got their million dollar bonuses from taxpayer bailouts and the Federal Reserve secretly pumped in $29 trillion over 31 months to shore up the failing trading houses on Wall Street and their derivative counterparties.Wall Street banks have rebuilt that derivatives doomsday machine today – a $168 trillion monster concentrated at four mega banks on Wall Street. Office of the Comptroller of the Currency, provided the following state of affairs as of March 31, 2021:These four banks are not the investment banking units of the Wall Street mega banks. They are the federally insured, taxpayer-backstopped, commercial banking units of these Wall Street behemoths. Per the chart below, JPMorgan Chase Bank, Goldman Sachs Bank USA, Citibank N.A. (the federally-insured unit of Citigroup), and Bank of America are sitting on a total notional (face amount) of $168 trillion in derivatives or 89 percent of the $189 trillion at all banks.

Note that the above numbers in the chart are “millions of dollars,” meaning that JPMorgan alone, with assets of just $3.2T, holds derivative bets totally $52.6 trillion dollars. It is levered more than 16x its assets. Reforms passed by Congress following the 2008 crisis and bank bailouts have been continuously eroded at the behest of the banks that want no constraints on their risk taking. Thus, the major US banks are once again exposed to catastrophic derivative losses.

When the next day of reckoning comes, the Fed will again bail the banks out with more printed trillions of dollars just as it did in 2000, 2008, 2019 and 2020. The Fed executes these bailouts through the New York Federal Reserve Bank. We have observed in the past that the NY Fed is not a government entity. It is a privately owned corporation. Its shareholders include JPMorgan, Citigroup, Morgan Stanley, Bank of New York Mellon and Goldman Sachs. Thus, when these banks periodically blow themselves up, they simply “bail themselves out” with money created by the Fed. How did this come to pass?

The story of how the Fed was created in total secrecy makes fascinating reading. The Creature From Jekyll Island, by G. Edward Griffin, describes how elite banking insiders concocted this scheme that purports to be a government entity but was designed to serve their interests. Only when you know how and why the Fed was created, can you understand why it acts the way it does. https://www.amazon.com/Creature-Jekyll-Island-Federal-reserve/dp/091298645X/ref=sr_1_1?crid=2LZVABHVJ5PH0&dchild=1&keywords=the+creature+from+jekyll+island+book&qid=1628261152&sprefix=jekyll+island+book%2Caps%2C170&sr=8-1

The Fed was ostensibly established to act as a “lender of last resort” to solvent banks suffering a temporary run on deposits. Its emergency loans were intended to bear a “penalty” rate of interest to discourage improvident borrowing. While the Fed’s stated goals have since expanded to include defending the dollar and supporting full employment, its principle goal remains saving the big banks from their own incompetence.

This raises the question of whether the mega Wall Street banks are worthy of continuing taxpayer support. You be the judge. More from the Martens:

Until 2014, no major Wall Street bank that held federally insured deposits had ever been charged with a felony in a century. That all changed on January 7, 2014 when the U.S. Department of Justice charged JPMorgan Chase with two criminal felony counts for its role in the Bernie Madoff Ponzi scheme. The bank had managed the business account for Madoff for decades and had even written to U.K. regulators that it suspected Madoff of running a fraudulent operation. It failed to share any such concerns with U.S. regulators. JPMorgan Chase admitted to the charges and received a deferred prosecution agreement.Less than one and a half years later, on May 20, 2015, the unthinkable occurred. JPMorgan Chase, the largest federally-insured depository bank in the United States, was charged with another felony count, bringing the new total to three felonies to which it had admitted guilt. This time the charge was being part of a bank cartel that was rigging foreign exchange markets. Another U.S. bank, Citigroup’s Citicorp was also charged with a felony count in the matter. Both JPMorgan Chase and Citicorp pleaded guilty to the charges and received a deferred prosecution agreement.The concept behind deferred prosecution agreements is that the bank pays a large fine, is humiliated in public, faces shareholder wrath, thus forcing the Board of Directors to sack its CEO and thus ending the bank’s life of crime. This has proven to be a quaint concept when it comes to Wall Street’s mega banks.Three felony counts into its life of crime and the Board of Directors of JPMorgan Chase still hadn’t sacked the Chairman and CEO, Jamie Dimon, who had been at the helm of the bank during all three counts. Then, in what can only be described as something out of an Orwellian dystopia, on September 29, 2020, the Justice Department leveled two more felony counts against JPMorgan Chase, to which it once again admitted guilt and received yet another deferred prosecution agreement.The two felony counts in 2020 were for wire fraud for manipulating trading in the precious metals and U.S. Treasury markets. The Justice Department brought only two felony counts despite the fact that its own charging document indicated that JPMorgan traders engaged in “tens of thousands of instances of unlawful trading in gold, silver, platinum, and palladium…as well as thousands of instances of unlawful trading in U.S. Treasury futures contracts and in U.S. Treasury notes and bonds….”Typically, these kinds of charges by the Justice Department arrive with great fanfare and a major press conference. But the legal team of JPMorgan Chase apparently used their clout and no press conference was held by the Justice Department as JPMorgan Chase racked up its fourth and fifth felony counts in the span of seven years – all under the tenure of Jamie Dimon.

JPMorgan (i.e., its shareholders) has paid fines of over $35 billion for the bank’s numerous frauds and crimes. Instead of giving him the boot, last year JPM’s board of directors rewarded Jamie Dimon with $31M in compensation. He has also received 9.3 million shares of JPMorgan stock in “performance bonuses” over the years, making him a billionaire. The bank recently announced he will receive another 1.3 million shares of stock to induce him to continue heading JPMorgan for another five years.

Is JPMorgan a Wall Street outlier? Sadly, not. Citibank’s parent, Citigroup, received $2.3 trillion in secret, cumulative loans from the Fed to bail it out during the 2008 sub-prime fiasco. It was insolvent at the time and therefore should not have been bailed out but shut down. It took an act of Congress to force the Fed to disclose the identity of the banks that it bailed out. Citigroup was the largest bank bailout in global banking history. It has been fined over $25 billion for its many crimes, frauds and misdemeanors. Here is a sampling from the Martens:

December 11, 2008: SEC forces Citigroup and UBS to buy back $30 billion in auction rate securities that were improperly sold to investors through misleading information.July 29, 2010: SEC settles with Citigroup for $75 million over its misleading statements to investors that it had reduced its exposure to subprime mortgages to $13 billion when in fact the exposure was over $50 billion.October 19, 2011: SEC agrees to settle with Citigroup for $285 million over claims it misled investors in a $1 billion financial product. Citigroup had selected approximately half the assets and was betting they would decline in value.February 9, 2012: Citigroup agrees to pay $2.2 billion as its portion of the nationwide settlement of bank foreclosure fraud.August 29, 2012: Citigroup agrees to settle a class action lawsuit for $590 million over claims it withheld from shareholders’ knowledge that it had far greater exposure to subprime debt than it was reporting.July 1, 2013: Citigroup agrees to pay Fannie Mae $968 million for selling it toxic mortgage loans.September 25, 2013: Citigroup agrees to pay Freddie Mac $395 million to settle claims it sold it toxic mortgages.December 4, 2013: Citigroup admits to participating in the Yen Libor financial derivatives cartel to the European Commission and accepts a fine of $95 million.July 14, 2014: The U.S. Department of Justice announces a $7 billion settlement with Citigroup for selling toxic mortgages to investors. Attorney General Eric Holder called the bank’s conduct “egregious,” adding, “As a result of their assurances that toxic financial products were sound, Citigroup was able to expand its market share and increase profits.”November 2014: Citigroup pays more than $1 billion to settle civil allegations with regulators that it manipulated foreign currency markets. Other global banks settled at the same time.May 20, 2015: Citicorp, a unit of Citigroup becomes an admitted felon by pleading guilty to a felony charge in the matter of rigging foreign currency trading, paying a fine of $925 million to the Justice Department and $342 million to the Federal Reserve for a total of $1.267 billion. The prior November it paid U.S. and U.K. regulators an additional $1.02 billion.May 25, 2016: Citigroup agrees to pay $425 million to resolve claims brought by the Commodity Futures Trading Commission that it had rigged interest-rate benchmarks, including ISDAfix, from 2007 to 2012.July 12, 2016: The Securities and Exchange Commission fined Citigroup Global Markets Inc. $7 million for failure to provide accurate trading records over a period of 15 years. According to the SEC: “CGMI failed to produce records for 26,810 securities transactions comprising over 291 million shares of stock and options in response to 2,382 EBS requests made by Commission staff, between May 1999 and April 2014, due to an error in the computer code for CGMI’s EBS response software. Despite discovering the error in late April 2014, CGMI did not report the issue to Commission staff or take steps to produce the omitted data until nine months later on January 27, 2015. CGMI’s failure to discover the coding error and to produce the missing data for many years potentially impacted numerous Commission investigations.”

Following the real estate mortgage fiasco, Chuck Prince, Citi’s CEO at the time, tried to justify the huge risks the bank was taking. He said, “When the music stops, in terms of liquidity, things will get complicated. But as long as the music is playing, you’ve got to get up and dance.” In other words, if other banks were making big money taking huge risks, Citi had to do so too. That is the sort of “leadership-thinking” at the US mega-banks and is why the next banking crisis will be far worse than the last one.

Of course, JPMorgan and Citigroup are not the only mega bank fraudsters. Wells Fargo has had to load up its stagecoach with $21 billion to pay its many fines, including $3B for fraudulently opening thousands of phony accounts for existing customers in order to stick them with millions of dollars in monthly fees. Since the year 2000 “Vampire Squid” Goldman Sachs has paid $16 billion in fines for its roles in selling toxic securities to investors, violating investor protection rules, violating the Foreign Corrupt Practices Act, mortgage abuses and numerous other banking rule violations.

Bloomberg reported that Bank of America, Citigroup, JPMorgan Chase and Wells Fargo have paid more in dividends since 2017 than their net incomes. The bank’s officers, being big shareholders, raked in those dividends.

From the start of 2017 through March, the four banks cumulatively returned about $1.26 to shareholders for every $1 they reported in net income. Citigroup returned almost twice as much money to its stockholders as it earned, according to the data, which includes dividends on preferred shares. The banks declined to comment.

The Martens add:

We need to pause right there for a moment because both Fed Chairman Jerome Powell and the Fed’s Vice Chairman for Supervision Randal Quarles have been telling Congress and the public for months now that these mega banks, which it is in charge of supervising, have “adequate capital” and are a “source of strength” in this crisis. There is no accounting alchemy in the world that can make Citigroup a source of strength if it’s been paying out twice as much money as it’s been earning for 3 ½ years.

Was it embarrassing for Jerome Powell, Chairman of the Fed, when three of the largest banks in the U.S. were recently deemed “not trustworthy” by the European Commission and were banned from participating in its historic European Union bond offering? Not likely. Paying fines for crimes and frauds is just a cost of doing business for the US mega banks. Who were the three miscreant banks barred from the bond offering? Citigroup, Bank of America and, of course…. J.P. Morgan. Who pretends to supervise these banks? The NYFed.

The Fed’s repeated bailouts of incompetent bankers creates what is known as “moral hazard.” In economics that means an entity has an incentive to take enhanced risks because it knows that it will not bear the full cost of potential losses. Chuck Prince felt comfortable continuing to “dance to the music” late into the night because he knew taxpayers would bail him out if the risks he was taking blew up in his face. He was right. The Fed bailed out Citi with over $2T in loans.

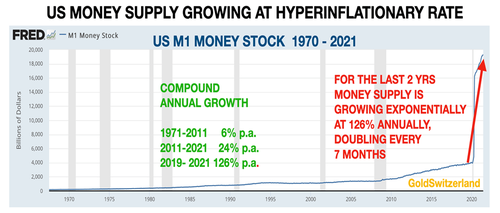

Explosive Growth of the US money supply

In order to bail out the mega-banks and support the US Treasury that never has enough money to pay its expenses, the Fed has created trillions of dollars from thin air. When the market is flooded with trillions of fresh dollars, prices inevitably rise to the disadvantage of consumers, especially those at the lower ends of the socio-economic scale. Jeff Bezos’ standard of living will not be affected by 5% inflation but those working at minimum wage jobs will be stressed to the limit.

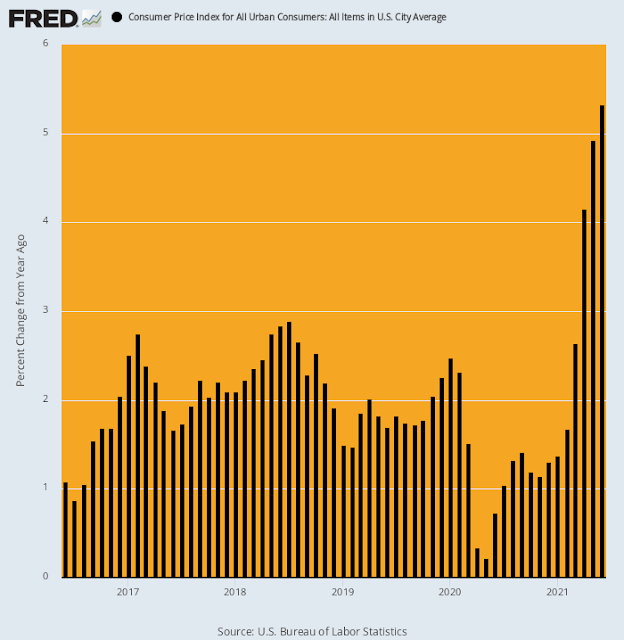

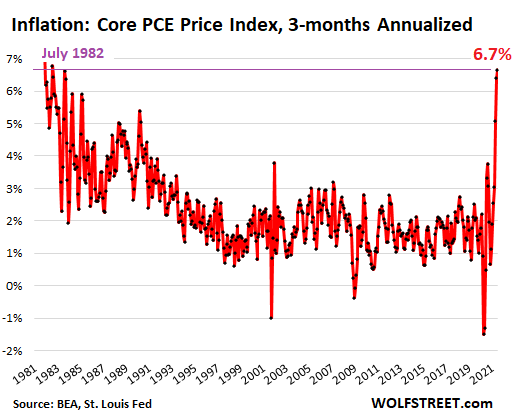

The next chart shows the effect of the Fed’s money surge on consumer prices.

CPI Growth for Urban Consumers

Every month, the Fed continues to buy $80B of Treasury securities and $40B of agency debt (Fannie Mae and Freddie Mac bonds) with newly printed dollars. It holds over $5.2 trillion of Treasuries (about 25% of all Treasuries outstanding) and $2.3 trillion of agency debt. The soaring CPI raises the question of why the Fed does not cut back on its money printing to stem the tide of price inflation. The reason is that it cannot do so. The economy is so dependent on a continuous flow of zero-cost money that any reduction will trigger a stock market collapse and deep recession. The Fed has painted itself into a corner. There is no way out. John Mauldin:

Decades of policy errors leave the Fed with no good options. All the choices are bad and they can only choose the least bad. Not a good position to be in, but it’s where they are. And the rest of us are with them, like it or not. I would like to go back to a time when we didn’t wake up in the morning wondering what the Federal Reserve would do. Its actions have distorted the economy, repressed savers, and made the wealth and income divide far greater than it should be.

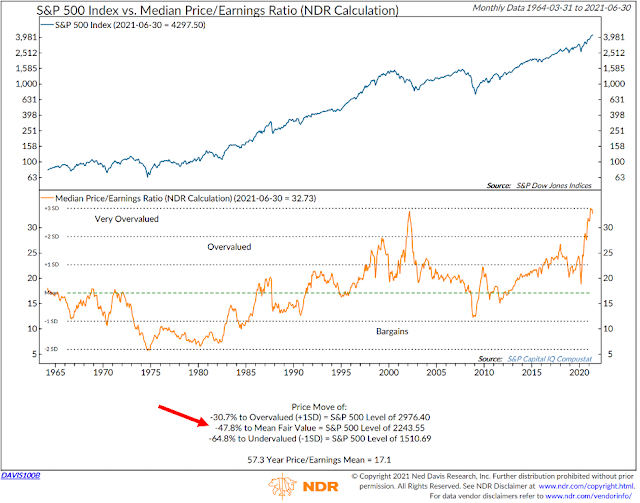

In addition to causing prices to rise in consumer goods, the torrent of new dollars from the Fed has also created stock market bubbles. The chart below from Ned Davis Research shows the steady rise in the S&P 500 in the top half, and the market’s median price-to-earnings ratio in the bottom half. History proves that when stocks fall below 16x P/E they tend to be bargains and when they rise well above that level they tend to be overpriced and subject to correction. The red arrow on the bottom of the chart shows that the S&P would have to correct almost 50% to reach “mean fair market value” and 65% to reach bargain value. The essential take-away from this is that stocks bought at high price-to-earnings ratios tend to have low-to-negative future returns.

Here is another way of looking at the market to assess whether it is seriously overpriced. This tracks the S&P (black line) and the index’s 50-month moving average (blue line). The index typically does not vary greatly from the 50-month moving average - until this year. It is now well out over its skis. While this does not ensure an imminent correction, it is a fair warning of one to come.

The Hidden Costs of the Fed’s Extreme Monetary Policies

The Fed’s twenty-year, ham-handed interventions in the markets do not come without consequences. Bill Bonner: “The fake interest rates/fake-money system discourages real saving and real investing (building factories… training workers… increasing real output) and favors short-term speculating, cockamamie gambling, and jackass politics.” Why does the voting public tolerate this? Mr. Bonner provides an old Adolf Hitler quote, “What luck for the rulers that men do not think.” If enough men (and women) thought about what the Fed has done and continues to do to our economy, they would demand an end to the debasement of the dollar. But they do not think about it, so prices will continue to rise leading to a demand for yet more hand-outs that will, in turn, exacerbate the problem rather than solve it.

Voters have not objected for two reasons: 1) those who have been enriched by the Fed’s actions are not about to complain, and 2) those who have been beggared by it do not have the slightest notion of what is happening to them. Of those who have been ostensibly benefitted by the Fed, many suffer from what is known as the “Money Illusion.” They focus on their growing numeric “wealth” while ignoring how little those dollars will buy in the future.

Graham Summers argues why price inflation will continue.

In 1776, two books were published in England that rocked the world. One was Adam Smith’s The Wealth of Nations. The other was Edward Gibbon’s Decline and Fall of the Roman Empire.Smith’s book wasn’t really about the wealth of nations. It was mostly about how states squander and destroy that wealth by costly interventions.Gibbon’s book wasn’t about the collapse of the Roman Empire. It was mostly Gibbon trying to puzzle out what in the heck took it so long.One thing we can learn from both of them: When it comes to monetary policy, history reveals that governments are unable to maintain the political discipline required to avoid funny money inflation.Even legal barriers aren’t enough. In the 1790s, during the French Revolution, legal limits on the amount of currency in circulation were imposed by the French Assemble. And to no avail. By hook or crook, short-term political meddling always finds a loophole.

Some things never change. Governments’ debasement of their currencies is one of those constants. They get away with it by misrepresenting the state of the economy and the purported benefits of their interventions - and by the compliant/complicit media that fail to challenge their misrepresentations.

In The Road to Serfdom, FA Hayek observed:

If all the sources of current information are effectively under one single control, it is no longer a question of merely persuading the people of this or that. The skillful propagandist then has the power to mold their minds in any direction he chooses, and even the most intelligent and independent people cannot entirely escape that influence if they are long isolated from all other sources of information.

Charles Hugh Smith describes the price we pay for inaccurate market information.

Markets are fundamentally clearing houses of information on price, demand, sentiment, expectations and so on--factual data on supply and demand, shipping costs, cost of credit, etc.--and reflections of trader and consumer emotions and psychology.If markets are never allowed to go down, the information clearing house has been effectively shut down. Whatever information leaks out has been edited to fit the prevailing narrative, which in this moment is "central banks will never let markets go down ever again, so jump in and ride the guaranteed Bull to easy gains."The past 12 years offer ample evidence for this narrative: every dip draws a near-instantaneous monetary-policy response that reverses the dip and gooses markets higher.That permanent monetary intervention distorts markets doesn't matter to participants. Who cares if markets have become a simulacrum of real markets that are now nothing but signaling mechanisms that all is well so buy, buy, buy? If gains are essentially guaranteed, who cares that markets are no longer information clearing houses?Indeed. There's no reason to care until the fatal spiral downward surprises us all. Here's an analogy of what happens when real information gets edited to fit a convenient narrative. Unfortunately, the patient has cancer, which is starting to metastasize, i.e. spread to other organs in the body. But unbeknownst to the patient, this accurate information is considered "bad news," so the test results and other information is carefully edited to show the cancer is actually shrinking--the exact opposite of what the actual facts reflect. The patient is naturally delighted with this false data because it appears he's on the mend and doesn't need any surgery or other drastic treatments.If participants don't have information that reflects actual conditions, they cannot help but make disastrous decisions. Falsified or heavily edited information is misleading, and so all decisions made on the assumption this information is accurate will be fatally skewed.

The Fed, our political leaders and the mainstream media are firehoses of misinformation. We need to search for the information that is being ignored or suppressed. When we do, it becomes increasingly obvious that the Emperor (Fed/ECB) has no clothes (i.e., viable plan to return the economy to a normal state of affairs where supply and demand determine interest rates and which businesses succeed or fail). Instead of free markets, what we have today are soviet-style, central planning committees - central banks - that call the shots and declare the winners and losers. As modern western economies continue to deviate from the principles of sound money, they hasten down the road to perdition. Stanley Druckenmiller, CEO of Duquesne Capital, recently wrote,

If I was Darth Vader and I wanted to destroy the US economy, I would do aggressive spending in the middle of an already hot economy… What are you going to get out of this? You’re going to get a sugar high, higher inflation, then an economic bust.

History proves that every centrally planned economy self-destructs. David Stockman pins the tail on the donkey.

[Powell] is not only a clueless bag of wind, but is also the poster boy for a camarilla of central bankers who have spent years wantonly violating every canon of sound money and economic rationality known to mankind, and are now so cocooned in a groupthink catechism as to be utterly delusional about the impact of their own policy actions. There is no other way to say it: The Fed has become a dangerous rogue institution which has usurped plenary power over the financial system based on implicit theories that will eventually and inexorably lead to a massive speculative blow-off, even as it sucks the vitality out of the main street economy in the interim.The implicit theory is brazenly simplistic: The Fed believes relentless credit expansion fosters higher economic growth and full employment; and that there is no practical limit as to how much debt the household, business and government sectors of the economy can tolerate or any notable adverse trade-offs which come from ever higher leverage ratios.Self-evidently, of course, lower interest rates foster more debt issuance. So when economic growth falters for any reason, the Fed’s action of first, only and unhesitating resort is to push rates ever lower. This ratcheting process has now gone on for more than three decades, and interest rates have for all practical purposes been obliterated. You would think by now, however, that these dunderheads would recognize that mega-debts are not an economic elixir, and that measured over any sustained period of time the Fed’s pro-debt/interest repression policies have been an utter failure.

Who pays the price for the Fed’s and ECB’s arrogant interventions? We all will. In part, we will pay for it with ever-higher prices due to their continuing debasement of our currencies.

© All rights reserved 2021

If you find this material interesting feel free to sign up to have it delivered directly to you by going to WorldViewInvesting.com, click on the top left corner icon and select the “Subscribe” button. We will not share your email with anyone. If you are not receiving issues, please check your spam/junk folder and then “whitelist” us.

Important Message: The foregoing is not a recommendation to purchase or sell any security or asset, or to employ any particular investment strategy. Only you, in consultation with your trusted investment advisor, can select the strategy that meets your unique circumstances, investment objectives and risk tolerance.