JEROME POWELL FINALLY GETS SERIOUS, CHRISTINE LAGARDE AND ANDREW BAILEY DITHER

President Biden, Jay Powell, Christine Lagarde (head of the European Central Bank), Boris Johnson and Andrew Bailey (head of the Bank of England) all vow to fight surging inflation. None will succeed over the long term. If investors understand why this is the case they will be far better positioned for what comes next. As is often the case, the best indicator of the future is the past. When we fail to take note of history we continue to be surprised by recurring events. History tells us what we need to know about government finance and its impact on prices and markets. Every financial crisis differs in some respects from others, but most have a common denominator. That is excessive individual, corporate and governmental debt resulting from maniacal central bank money printing.

There have been hundreds of fiat currencies (those not backed by something of intrinsic value such as gold or silver) that have disappeared and for the same reason – overprinting by those in government in an effort to get “something for nothing.” Examples include the French assignat that was issued during the French Revolution of 1789. It was originally backed by lands seized from the Catholic Church but then was transformed into a fiat currency. It became nearly worthless by 1796 after being printed in excess to pay for the war of 1792 and support the nobility. It was replaced with the mandats territoriaux that was soon replaced with the napoleon. Another example is the bolivar. In 1879 the Venezuelan bolivar replaced its predecessor, the massively devalued venezolano. After the bolivar lost most of its value, it was replaced with the “hard bolivar.” Following further money printing that led to hyperinflation in 2018 it was replaced with the “sovereign bolivar” (exchange rate 100,000/1) followed by yet another change in 2021 in which six zeros were lopped off of the bills. These examples give credence to Voltaire’s observation that, “Paper money eventually returns to its intrinsic value – zero”.

Two of the longer serving currencies are the British Pound and the US Dollar. Both began as “hard” (gold-backed) currencies and evolved into fiat currencies for political expediency to pay for wars, waste and social benefits intended to keep the support of the voting public. Those in political power always want to spend more to benefit themselves, their crony friends and to get re-elected than citizens are willing to pay in direct taxes. Politicians know that when taxes become unbearable, revolutions ensue so taxes are usually kept in check. Thus, the insiders must fall back on the “indirect tax” of inflation to subsidize their reckless spending. Fortunately for them, not one in a million of the public understands the cause of rising prices (excessive money printing) and are encouraged by politicians to blame “greedy businessmen” as the source of their pain. Of course, when input costs (labor, transportation, raw materials, administration) increase for businesses due to the effects of monetary inflation, they must raise their prices to cover those increased costs. But making businesses the boogie-man diverts the people’s attention from the real agents of pain, their political leaders.

Politicians know that they will never get elected to office, or be retained in office, if they run on a platform of fewer benefits for taxpayers and higher taxes. So, they promise ever-more benefits without raising taxes to pay for those benefits. They expect to meet the cost of those benefits by printing money (e.g., by the Fed, ECB, BOE). In the US this has been going on for the last fifty years leading to a national debt of $30 trillion most recently resulting from the money-printing extravaganza since 2000. That is why price inflation is now at a forty-year high.

As inflation inevitably soars following decades of money printing, voters begin to complain and demand that politicians “do something” about it. Only when inflation has become a huge problem (evidenced by rising voter anger) does anyone in government admit that there might be a problem. Recall Fed chairman Jay Powell’s refusal to admit for many months that there was a problem, insisting that price inflation was “modest,” “transitory,” and would soon resolve itself – even as it continued to rise month after month. Former Fed chair and now Treasury Secretary Yellen echoed his position. Both have since been forced to admit that they were clueless then but insist they have the solution to the problem - that they themselves created. They propose to raise interest rates to cool rising prices. However, current rates remain in deeply negative territory and are expected to remain that way through the end of 2024. Neither Powell nor Yellen appear to understand the simple proposition that negative real rates of interest (interest rates less the rate of price inflation) are incompatible with a healthy economy. Jim Grant, noted publisher of Grant’s Interest Rate Observer, writes,

Today’s rates, the lowest in 4,000 years, harm savers, advantage speculators, misdirect capital and perpetuate the unnatural lives of failing businesses that, by rights, ought to leave the marketplace to more capable competitors. We observe that radical monetary policy begets more radical policy and low rates, still lower rates. Repeated monetary interventions have fostered financial fragility, slow growth and heavy indebtedness.

All of these bad consequences that we now face were readily foreseeable effects of the incompetent monetary policies foisted upon western economies by their central banks. Now those central bankers are scrambling to undo the damage. Let’s review their work history:

The Greenspan Fed ginned up the idea to cut interest rates following the dotcom bust to create a housing bubble in order to take over from the imploded stock market bubble. This worked, and we got a housing bubble, to which the Fed responded by raising interest rates again to over 5%, which worked and caused the housing bubble to implode, which triggered the mortgage crisis, which performed a rug-pull under the over-leveraged banks, upon which the Fed rolled out its new dual-weapon QE and 0% interest-rate policy, which worked, and it inflated all asset prices, bailed out the bondholders and stockholders of the banks, and soon it triggered the next housing bubble, but much more magnificent than anything before. Wolfstreet

Nevertheless, the US Fed has recently raised interest rates three times (0.25%, 0.50% and 0.75%) to what is now a range between 1.5%-1.75%.[1] That, we are told, will put the brakes on prices that are rising at an 8.6% pace. A fifth grader could calculate that real interest rates are still negative - to the tune of nearly -7%! Thus, the Fed is still engaging in extreme monetary accommodation (is “dovish” and not “hawkish”). It announced that it will begin to slow the amount of bonds it is buying (QE) - but it will continue to buy them. Only in the world of central bankers would these steps be deemed to be serious efforts to plunge a wooden stake through the heart of price inflation. It is also worth remembering that the Fed has never succeeded in lowering its balance sheet by more than $750B before being forced to resume QE due to a collapsing stock market and/or recession. Will this time be different? Michael Lewitt writes,

[Former Treasury Secretary and now professor Lawrence] Summers confirms that economic policy is set by people guided by flawed models. We watch the Fed stumble from one policy failure to another, creating market bubbles, massive wealth inequality, and runaway debt and speculation with few if any complaints from business and political leaders. Instead, our so-called elites benefit from this intellectually and morally corrupt regime without a thought about the future destruction being wrought on America’s (and the world’s) economy by their fellow empty suits.Having contributed mightily to the highest inflation in 40 years, the Fed has limited tools to fight it. The only thing that will lower energy and labor costs is an economic slowdown. A recession is both an economic necessity and a near-certainty. Corporate earnings, inflated by phony non-GAAP earnings adjustments, are declining and there is only so much managements can do to fake their way through a slowdown (especially with so much debt on their balance sheets). And consumers, despite the incessant stream of bullsh*t they are fed about their strength, are maxing out their credit cards and struggling with nauseatingly high energy, food and housing costs (all conveniently excluded from government inflation statistics), are going to reduce their spending (and are telling the University of Michigan [public opinion poll] that they are decidedly not happy).

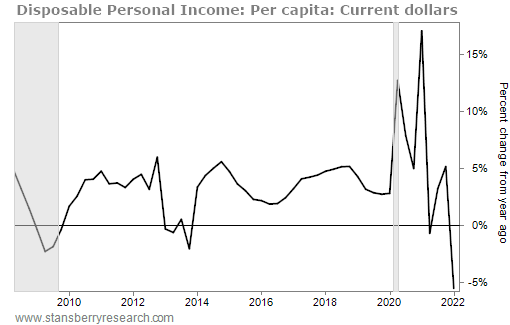

Lewitt’s assessment is confirmed by dramatically falling per-capita disposable income.

Bear in mind that the headline government-issued CPI inflation report intentionally omits the cost of food and energy – expenses that consumers incur daily - and it grossly underreports the cost of housing. ShadowStats.com estimates price inflation to be between 15%-18%. It calculates the cost of living as done by the government in the 1980’s without “hedonic” adjustments now used to intentionally underreport the true rising cost of living (see link below)[2]. This ignores food price increases such as:

- Fresh vegetables: 6.4%

- Fresh fruits: 8.5%

- Beef and veal: 10.2%

- Dairy and related products: 11.8%

- Fish and seafood: 12.2%

- Cereals and cereal products: 12.8%

- Baby food: 12.9%

- Pork: 13.3%

- Coffee: 15.3%

- Poultry: 16.6%

- Fats and oils: 16.9%

- Eggs: 32.2%

- Electricity service: +12.0% over the last year (y/y)

- Utility natural gas to the home: +30.2% y/y

- Total Energy CPI: +34.6% y/y

- Gasoline: +48.7% y/y.

Biden, Powell and their European counterparts insist that they have the best of intentions to guide our economies away from the shoals of recession. Janan Ganesh, writing at the Financial Times, reminds us that, “a fool is no less dangerous for meaning well.” These leaders were oblivious to the growing threat of today’s high inflation and they actively misrepresent its cause and extent. The economic models they constructed and relied on were patently flawed. Should we now believe they will be able to reverse course without causing new and unforeseen problems?

Søren Kierkegaard noted that our dilemma is, “life can only be understood backwards; but it must be lived forward.” We can readily see what our government officials have done to create this disaster but it is difficult to anticipate all of the consequences of their past (and future) incompetence. While inflation attracts the public’s attention today, an even more pressing problem is staggering levels of debt – both public and private. Private debtors who are well in over their heads have the option of defaulting on their obligations and declaring bankruptcy. How do governments address their unpayable debts? Late economist Murray Rothbard describes their historic strategy.

Devaluation of the currency, after all, is how nations throughout history have managed to wriggle out of debts they couldn't pay. Watering down the currency is a time-honored way of paying off your debts with money that's worth less now than it was when you ran up the bill.

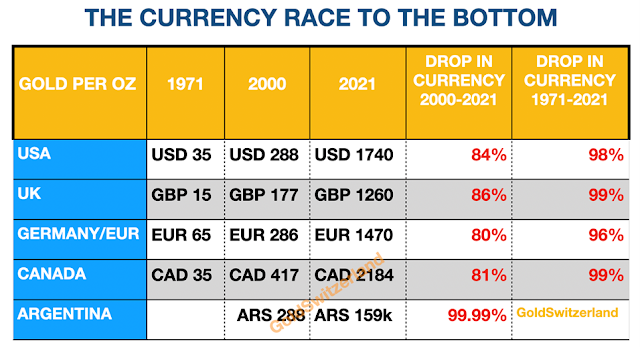

True to form, since 2000 the Fed has debased the dollar by nearly 50%! Since the Fed’s creation in 1913 the dollar has lost 98% of its purchasing-power. This sorry history convincingly demonstrates that ongoing debasement of the dollar is not an operational “aberration” but has been the Fed’s premier policy for 109 years. As they say in the world of software development, debasement of the currency is not a “bug” in their program it’s a “feature.”

Rothbard relates a particularly heinous act by President Roosevelt.

In 1932, Franklin Roosevelt required all Americans to turn in their gold. If you refused to do it, you'd be put in jail for 10 years and fined nearly $200,000 in today's money.Roosevelt compensated people who turned in their gold at $20 an ounce. But then he set the price of gold [to the dollar] at $35 an ounce. Since the value of the dollar was still linked to the price of gold at that time, he thereby devalued the U.S. Dollar by 42%.

Though never portrayed in history books as such, the direct and intended effect of Roosevelt’s action was to confiscate 42% of the value of all of the coins seized from the people. If your neighbor or banker did that to you he would go to jail. Inflation does the same thing to you. Are you beginning to get the picture that you and your government are not on the same team?

Rothbard also refuted the Fed’s monetarist theory explaining why “printing money” does not make us richer,

What makes us rich is an abundance of goods, and what limits that abundance is a scarcity of resources: namely land, labor and capital. Multiplying coin will not whisk these resources into being. We may feel twice as rich for the moment, but clearly all we are doing is diluting the money supply. As the public rushes out to spend its newfound wealth, prices will, very roughly, double — or at least rise until the demand is satisfied, and money no longer bids against itself for the existing goods.

Those in government appear not to understand this obvious fact. We submit that they well understand it but cannot resist the temptation to enrich themselves and their friends at the expense of the multitude (you). But there is a consequence for this fraud as Bill Bonner explains,

Once you begin living on “printing press” money, you soon become dependent on it. Then, you need to print more and more just to keep from slipping backwards. There’s no example in history where printing-press money has actually made an economy better off – none. Nor has it ever made people a penny richer. Instead, it always leads to poverty, chaos, inflation, social upheaval, and corruption. But this inconvenient detail will stop neither Republicans nor Democrats, neither the Fed nor Congress, neither Trump nor Biden.The Fed only pretends to fight inflation by raising rates. The feds inflate by buying bonds. Buying bonds keeps interest rates low. With $85 trillion in total debt, every 1% increase in real interest rates costs the nation $850 billion in extra debt service. A 5% increase (back to more normal rates) would cost $4.2 trillion. If the feds stop printing money and allow Treasury yields and interest rates to return to normal, in a matter of seconds, the whole flimflam blows up.

While a few of the insider elite in government know that there will be a day of reckoning for their monetary mischief they intend to leave office before it arrives to avoid being hung from nearby yardarms. Unfortunately, the vast majority of people in government have no understanding of how governmental expenses are financed.

In theory, inflation “cures” the problem of the massive government debt. A negative 3% real yield brings down the real value of a government’s debt load by 46% over 20 years. A negative 5% real yield brings it down by 64%. That is why government bonds are often referred to as “certificates of confiscation.” However, in practice, prolonged high inflation often brings down the government either through elections or revolutions.

We have shown this dated chart to you before. It helps to remind us what all governments have really been up to and will continue to be up to.

The aforementioned Larry Summers, former U.S. Treasury secretary and now Harvard University professor, recently told Bloomberg Television that economists are once again reverting to the flawed “monetarist theory” that governments need to “stimulate” more consumer spending (“increase aggregate demand” in economist terms) in order to grow their economies. That is nonsense Summer says.

[We do not need people] to buy more stuff even if they don’t need it. There are millions of storage facilities across the nation warehousing crap people have bought and have no room for. They don’t need more stuff. They need less. Instead of buying more stuff, people are being forced to save more to make up for the niggardly interest they earn on their savings. Who’s fault is that? Central banks. Economists decry the “savings glut.” As if people saving for their future is an evil instead of a worthy goal. Savings provide the money to banks to lend to businesses. More savings is more money available for loans.

In addition to savaging savers for the last twenty years, the Fed and other central banks have also been actively distorting the securities markets. Whenever markets begin to stumble, they rush to the rescue with another massive injection of newly printed money. The heavy-hitter insiders in the markets have learned to game this response to their great personal advantage. Charles Hugh Smith expresses his concern.

Markets are fundamentally clearing houses of information on price, demand, sentiment, expectations and so on--factual data on supply and demand, shipping costs, cost of credit, etc.--and reflections of trader and consumer emotions and psychology.If markets are never allowed to go down, the information clearing house has been effectively shut down. Whatever information leaks out has been edited to fit the prevailing narrative, which in this moment is "central banks will never let markets go down ever again, so jump in and ride the guaranteed Bull to easy gains." The past 12 years offer ample evidence for this narrative: every dip draws a near-instantaneous monetary-policy response that reverses the dip and gooses markets higher.That permanent monetary intervention distorts markets doesn't matter to participants. Who cares if markets have become "markets," simulacra of real markets that are now nothing but signaling mechanisms that all is well so buy, buy, buy? If gains are essentially guaranteed, who cares that markets are no longer information clearing houses?There's no reason to care until the fatal spiral downward surprises us all. Here's an analogy of what happens when real information gets edited to fit a convenient narrative:Unfortunately, the patient has cancer which is starting to metastasize, i.e. spread to other organs in the body. But unbeknownst to the patient, this accurate information is considered "bad news," so the test results and other information are carefully edited to show the cancer is actually shrinking--the exact opposite of what the actual facts reflect.The patient is naturally delighted with this false data because it appears he's on the mend and doesn't need any surgery or other drastic treatments.If market participants don't have information that reflects actual conditions, they cannot help but make disastrous decisions. Falsified or heavily edited information is misleading, and so all decisions made on the assumption this information is accurate will be fatally skewed.

Or as Ayn Rand succinctly put it, “We can ignore reality, but we cannot ignore the consequences of ignoring reality.”

It is easy to see what all governments, most businesses and many individual investors have done in the face of low interest rates and printed money. They have eschewed savings and liquidity in order to “maximize their returns.” But not every business has fallen into this trap. Warren Buffet was recently challenged by an interviewer to justify why he keeps so much money in cash or near cash form. He explained,

[Berkshire] always has $20 billion or more in cash. It sounds crazy, never need anything like it, but someday in the next 100 years when the world stops again, we will be ready. There will be some incident, it could be tomorrow. At that time, you need cash. Cash at that time is like oxygen. When you don't need it, you don't notice it. When you do need it, it's the only thing you need. We operate from a level of liquidity that no one else does. We don't want to [be dependent] on bank lines [of credit].

He does not want to be dependent on bank lines of credit because those lines can suddenly become unavailable as happened during prior financial crises in 1998, 2000, 2008 and 2020. It might be at just such a time he could pick up a great company at a distressed price – if he had the cash immediately available to him. It is tough to hold cash when inflation is active but cash is the ultimate insurance policy. The premium you pay for that insurance is the rate of inflation. But having it allows you to sleep at night during the worst of times and make great purchases when they become available.

The Fed Is Not Alone In Favoring Inflation

The Fed, ECB and Bank of England speak in terms of orchestrating a “soft landing” for their economies that permits a strong economic recovery without suffering any pain. In that none of them foresaw the present crisis, the chance they will come up with the magic formula to “solve” this problem of their own making is not great. The ECB holds €5 trillion of bonds it bought to support the EU countries during the 2008 and Covid crises. Its interest rate is nominally 0.5% negative but with price inflation of over 8% it is -8.5%. Christine Lagarde (president of the ECB) has been toying with the idea of raising rates 0.25% in July and 0.5% in September. Those increases would not bring rates anywhere near positive territory and therefore would not blunt inflation. The ECB recently held an emergency meeting after which it sought to lessen fears that the eurozone might be headed to another debt crisis by saying it would seek new ways to reduce surging borrowing costs. There are only two ways to do that: lower interest rates into more negative territory (further exacerbating price inflation), or printing more money to make available for lending (further exacerbating price inflation) confirming that she has learned absolutely nothing over the last decade.

The ECB also holds hundreds of billions of euros of government bonds that are losing some 7% a year to inflation and corporate bonds for which there was no market. To whom will the ECB sell them? There are growing interest rate spreads between the German and Club Med government bonds. Italy’s bond yield recently exceeded Germany’s by 2.25%. It was only able to keep the spread that low for the last decade by selling its unwanted bonds to the ECB. If the ECB pulls back as a buyer, that yield spread will soar creating an existential financial crisis for Italy. Spain and Portugal have similar problems. Had those countries faced the music in 2008 they would have been forced to address their fiscal problems then. Instead, the ECB enabled them to avoid confronting their ever-growing problems for a decade. Their day of reckoning may be sooner than expected.

The Bank of England recently admitted that UK inflation will hit 11% this year but it is resisting calls for a steep increase in interest rates to curb the rising cost of living in favor of a fifth 0.25% rise. Like the Fed, the ECB and BOE have no good options. The pain of adjustment may come sooner or it may come later but it will come. These central banks will do all in their power to try to make it come later.

The Bank of Japan continues to devalue the yen in its effort to make Japanese exports more attractive. The yen is now above 135 to the dollar exceeding a 20-year low. Japan suffers from a shrinking population and an antipathy to immigration. As older workers age-out of the work force, there are not sufficient younger people to replace them and those leaving the work force begin to sell their stocks and other investments to support their retirements. This pressures stock prices to the downside. The BOJ looks to inflation of its money supply as the answer to these problems. David Stockman suggests what may come next,

By imperiously violating over the last 30 years every law of sound finance, honest money and common sense that the world had learned over the centuries, the central bankers have ended up creating a monster which will bring on their own demise. And none too soon.

The US has allowed career politicians and academic economists - both with no grasp of how the economy really works - to manage the massive and intricate $20.5 trillion US economy. Like the Fed, the ECB, BOE and BOJ were never designed to be ringmasters of their economies and they are not qualified or competent to do so. Yet, some in the US Congress want the Fed to assume the additional role of fighting “climate change” – another subject about which they know absolutely nothing. We are reminded of Thoreau’s comment that “we will have the worst government we are willing to endure.”

Final Thoughts

While the news in the world is terribly grim (thousands of Ukrainian deaths and vast destruction, inflation, mass murders, decaying cities, incompetent government officials) it is worth taking stock of how incredibly lucky we are to be living in present times where we are not required to labor dawn to dusk hunting and gathering our food supply and finding shelter from the elements and wild beasts. Thankfully, the world does not consist of just finance and politics.

“I, not events, have the power to make me happy or unhappy today. I can choose whichit shall be. Yesterday is dead, tomorrow hasn’t arrived yet. I have just one day, today, and I’m going to be happy in it.” Groucho Marx“Twenty years from now you will be more disappointed by the things that you didn’t do than by the ones you did do. So, throw off the bowlines. Sail away from the safe harbor. Catch the trade winds in your sails. Explore. Dream. Discover.” Mark Twain

1 - The Fed only has the ability to raise or lower the “Federal Fund Rate.” That affects the rate banks pay to borrow surplus reserve assets on an uncollateralized basis. It does not directly affect bank deposit, auto loan and credit card interest rates.

2 - http://www.shadowstats.com/alternate_data/inflation-charts

If you find this material interesting feel free to sign up to have it delivered directly to you by going to WorldViewInvesting.com, click on the top left corner icon and select the “Subscribe” button. We will not share your email with anyone. If you are not receiving issues, please check your spam/junk folder and then “whitelist” us.

Important Message: The foregoing is not a recommendation to purchase or sell any security or asset, or to employ any particular investment strategy. Only you, in consultation with your trusted investment advisor, can select the strategy that meets your unique circumstances, investment objectives and risk tolerance. © All rights reserved 2022