THE SUFFOCATION OF THE MIDDLE CLASS

We have written frequently about the harmful effects of government policies on the middle and lower classes throughout the Western world. Wage gains never keep pace with rising inflation. Ever more authoritarian controls over the public constrain their freedoms and limit their opportunities. No one in politics takes responsibility for these outcomes. Rather, those in power appear to be doubling down in their efforts to further enrich the elite at the expense of the workers who produce the goods and provide the services. A LendingClub report found that nearly two-thirds of the U.S. population now lives paycheck to paycheck, up from 61% at the end of the last year. Bankrate.com reports that three-quarters of respondents say that price hikes have hurt them financially. It is not their imagination. The US government admits to soaring inflation through their consumer price index (CPI) reports but the real numbers are far worse.

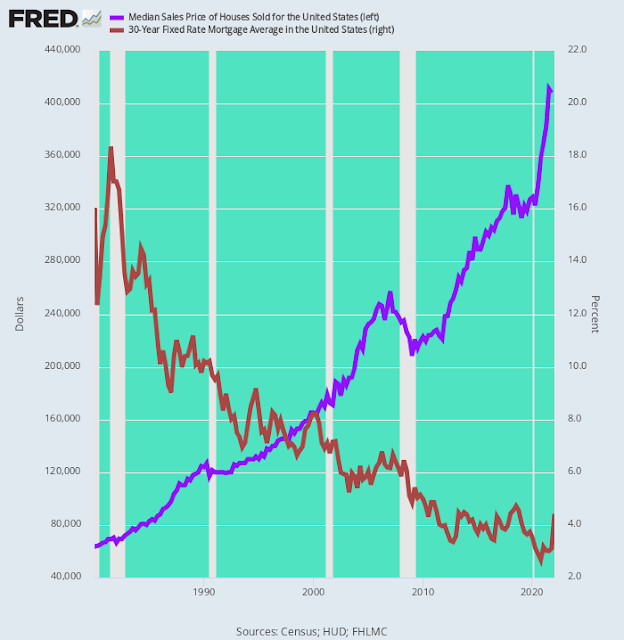

The CPI jumped 8.5% in March (over last year) while the producer price index rose 11.2%. Rapidly rising producer prices quickly find their way into consumer prices. Housing prices have made homes an impossible dream for a growing segment of the population and rising mortgage rates will not help. The chart below shows that the average price of a US home was $60,000 in 1980 but was recently over $410,000 (blue line). A major contributor to housing price inflation was ever-cheaper mortgage rates (red line).[1]

If rates continue to rise as promised by the Fed, home prices can be expected to fall and those who bought at the top may find themselves with a house worth less but with a still enormous mortgage. That will mean that banks who wrote those mortgages will be under-secured as happened during the housing debacle of 2007-8. Do not lose sleep worrying about the banks. The Fed will bail them out again with newly printed trillions of dollars as it has done before.

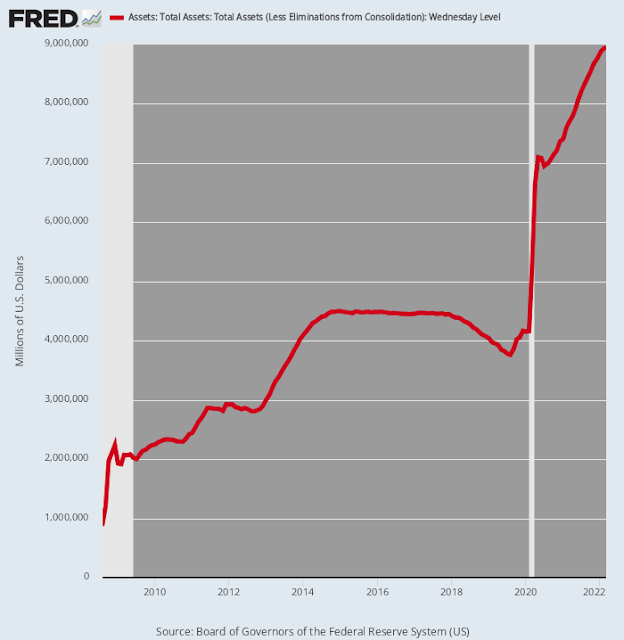

How did mortgage rates get so very low? The Fed began buying enormous quantities of mortgages rapidly becoming the world’s biggest “savings and loan” institution. It owns very long-term (30 year) fixed rate mortgages, and neither “marks them to market” (adjusts their value on its balance sheet to reflect the fluctuating values of the underlying properties) nor hedges its extremely large interest rate risk (the value of the mortgages falls as rates rise). Through FannieMae, Freddie Mac, and Ginnie Mae, the US government guarantees some $8 trillion of mortgage debt. As of March 2022, the Fed owned $2.7 trillion of mortgage backed securities. Thus, about a quarter of all the mortgages in the country are underwritten by the Fed and have become 30 percent of its total assets. Who will bail out the Fed during the next housing crisis? Here is a chart showing the astonishing growth of its assets purchased with printed money between 2008 and the present.

As the Fed printed this $8 trillion the US economy grew by approximately $9 trillion. Stated differently, the Fed paid for 88% of the growth of GDP. You might ask yourself if this is a viable business model. It is essentially MMT, Modern Monetary Theory, that argues we can print money to pay for whatever we want up to the point that inflation takes off. Well, inflation has taken off, so this should be the end of money printing - but it will not be. Therefore, consumer prices will continue to rise over the long term. These charts reflect the difference between “CPI inflation” as calculated by the government (red lines) and real inflation (blue lines), stated both as 1980 based (left) and 1990 based (right).

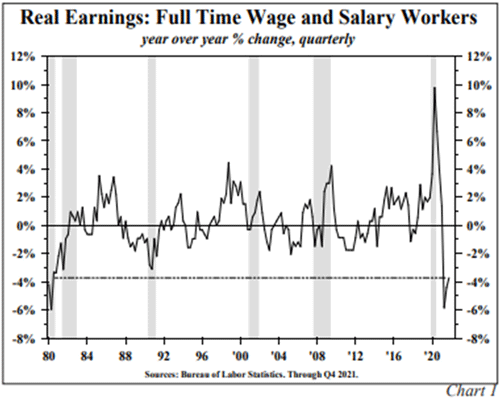

The effect of this price inflation on workers has been dramatic. Real earnings for wage and salary employees has fallen precipitously.

Fed Chairman Jerome Powell assures us that the Fed can engineer a “soft landing” meaning that it can lower inflation while not adversely affecting employment and the general economy. It plans to do this by pushing the lever of interest rates higher and off-loading the bulk of its balance sheet assets - Treasury and GSE (government sponsored entity) bonds. The Fed employs over 400 Ph.D. economists, so - we are told - we can all feel confident that it knows what it is doing. History refutes that premise. Those brilliant economists added $8 trillion to the Fed’s balance sheet while telling us it would have no effect on prices. Ben Bernanke said in January 2008, on the eve of the Great Financial Crisis, that “The Federal Reserve is not currently forecasting a recession.” David Stockman has asked, “if Bernanke [and his army of PhD economists] did not know that the deepest recession in the post-war period was underway, why would anyone think the Fed has a clue about the state of the domestic and global economy or the capability and wherewithal to micro-manage its course?” Chairman Powell told us that 2% inflation was what the nation needed and the Fed would not rest until it achieved that goal. As inflation pushed toward 3% he assured us that it was “transitory.” When it pushed to 4% he again insisted that it was “transitory.’ When it got to 5% he meekly agreed that it was time to retire the phrase “transitory inflation.” As it continued to push up to 6%, then 7% then 8% he continued to assert that the Fed is well equipped to address the problem. What the foregoing history suggests is that the Fed is clueless about how the economy actually works and that its vaunted “stochastic econometric models” are deeply flawed.[2]

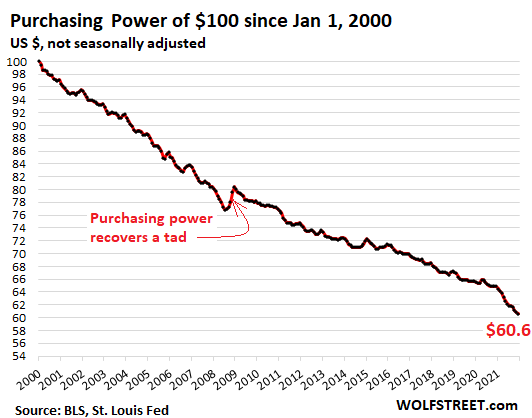

The Fed’s number one task is “price stability.” Real inflation rages at 13%. The Fed’s second task is to maintain the value of the dollar. The dollar has lost 40% of its value since 2000.

Based on this sorry history, why would any investor believe that the Fed will be able to successfully engineer a “soft landing” of the economy?

When and how did the Fed go wrong? That would take a very long time to explain. But Mises.org recently focused on a major flaw in its strategy. The Fed mistakenly sees an important relationship between inflation and employment, as argued by proponents of the “Phillips Curve.”

The imbalance between those who benefitted and those who were harmed from the monetary and fiscal policies pursued over the last two years is abundantly clear. The 8.5% inflation rate has dramatically lowered the standard of living of over 170 million individuals. When this circumstance is compared with the accomplishment of the objective by monetary and fiscal authorities to lower the unemployment rate from a recession high of 14.7% in April of 2020 to 3.6% today, the fallacy of twin mandates is abundantly clear. The lowering of the unemployment rate reflected the addition of 20.4 million jobs. Is it a fair balance to help 20 million individuals at the expense of permanently harming 180 million? The flawed dual mandate of inflation and unemployment stems from the basic fact that no stable trade-off exists between wage increases and the unemployment rate. In short, by relying on the Phillips Curve, the Fed avoids developing a strategic view of its role and the complex world in which it operates. Volcker explained publicly and to the Fed staff that the Phillips Curve was unreliable and not useful. Alan Greenspan was less outspoken, but he also rejected Phillips Curve forecasts as unreliable. After Greenspan left the Fed, the staff re-established the focus on the Phillips Curve, one of the central dogmas of Keynesian economics. When inflation is tolerated, it undermines growth and leads to increased calls for government intervention, thereby pushing countries further in the direction of command-and-control economies. The share of the government sector, with its negative multipliers, increases, while the share of the private sector, with its positive multipliers, declines. This reinforces the upward trend of inflation, perpetuating the cycle.

Dare we hope that our elected officials will save the day? They assure us that all is well - and that anything “not well” is not their fault. Joe Biden recently asserted that soaring US inflation is the fault of Vladimir Putin.

What people don’t know is that 70 percent of the increase in inflation was the consequence of Putin’s price hike because of the impact on oil prices. Seventy percent!

Biden fails to mention (forgot? never knew?) that inflation was rising well before Russia invaded Ukraine. Since the President is not a source of useful information perhaps we can look to our Congressional leaders to speak the truth. Speaker of the House, Nancy Pelosi, recently provided the following economic insight,

When we’re having this discussion, it’s important to dispel some of those who say, well it’s the government spending [that is causing inflation]. No, it isn’t. The government spending is doing the exact reverse, reducing the national debt. It is not inflationary.

Ms. Pelosi did not explain the magic by which government spending of trillions of dollars it does not have is “reducing the national debt” and “fighting inflation.” Shockingly low approval ratings reflect the public’s opinion of these political leaders. However, they are not alone in noting the scope of the problem. Daily Telegraph (UK) editorial writer Nile Gardiner wrote,

It is amateur hour on the world stage from the Biden Presidency. His visit to Europe was a train wreck, from his bizarre press conference in Brussels to the ad-libbed final words of his speech in Warsaw. At times Mr. Biden looked dazed and confused, struggling to command his sentences, and drifting into incoherence. The messaging was muddled, forcing even the president’s top officials to disown their own leader’s comments.On no fewer than three separate occasions, Biden’s own staff had to clarify or even refute the words of their commander in chief. Biden officials had to explain to the world’s media that he was not calling for US troops to go into Ukraine, that the United States would not respond to Russia with chemical weapons if Moscow used them, and that the Biden administration was not seeking regime change in Moscow.Biden in Brussels looked way out of his depth. There was no talk of winning in Ukraine, no promise to work with allies in substantially strengthening military assistance for the Ukrainian military. Biden looked weak, disorganized and even cognitively impaired at times. He does not inspire faith in US leadership, particularly at a critically important moment in time.Shamefully, Biden is happy to partner with Putin's tyrannical regime in getting a new nuclear deal with the world's biggest state sponsor of terror in Iran, one that will allow vast sums of money to flow to Tehran to fund terror groups like Hezbollah. This is a staggering act of sheer hypocrisy.

Of course, we should graciously overlook mere slips of the tongue. But Biden’s mental state is fairly at issue. He often appears to be confused, has repeatedly introduced Kamala Harris as “President Harris,” recently introduced his wife as the former vice-president under Obama and frequently tells the fanciful stories of having been an over-the-road truck driver and that their house burned to the ground around them. Do not mistake us as political partisans. We hold politicians of all stripes in equal low regard. What is so troubling is the lengths to which people will go to justify/excuse/explain away their favored politician’s evident shortcomings. Republicans did it with Trump and Democrats do it with Biden. Excusing incompetence, boorishness, autocratic conduct, absurd fiscal proposals, arrogant foreign relations, and turning a blind eye to ongoing social disintegration are not helping to move the ball forward.

What about the US Congress as a whole? Will it see the nation through these troubled times? David Stockman recounts its recent achievements.

In just the last 18 months, Congress has enacted $7 trillion of new spending for the Covid-Lockdown bailouts and the Biden infrastructure bill. Those enormous sums represent breathtaking overkill: They actually amount to 8.8X the $800 billion loss of GDP during the last six quarters. It’s also $54,000 for every single household in America.Yet they are not done. The so-called $1.8 trillion compromise on Biden's still pending social entitlements and green energy boondoggles will actually cost more than $4 trillion over the next decade when you remove the accounting gimmicks.Indeed, there is nothing like this bacchanalia of Washington spending in all of American history---including during the New Deal and LBJ's "guns and butter" excesses of the 1960s. Moreover, this potential total of $11 trillion of new spending was rushed through the Congress with virtually no hearings or expert analysis---meaning that Washington uncorked $85,000 per US household of new spending without the slightest regard for the long-term economic and fiscal consequences.Likewise, the Fed's balance sheet has erupted from an already bloated $3.8 trillion in August 2019 to $8.8 trillion at present. During the same 27-month period, the publicly-held Federal debt rose by nearly $5.2 trillion.This means nearly 100% of Washington’s explosion of borrowing and spending is being monetized----that is, financed with Fake Credits snatched from thin air by the mad money-printers at the Fed.But the laws of sound money, fiscal rectitude and economic gravity can't be defied indefinitely. There will eventually be a horrible reckoning, possibly soon.

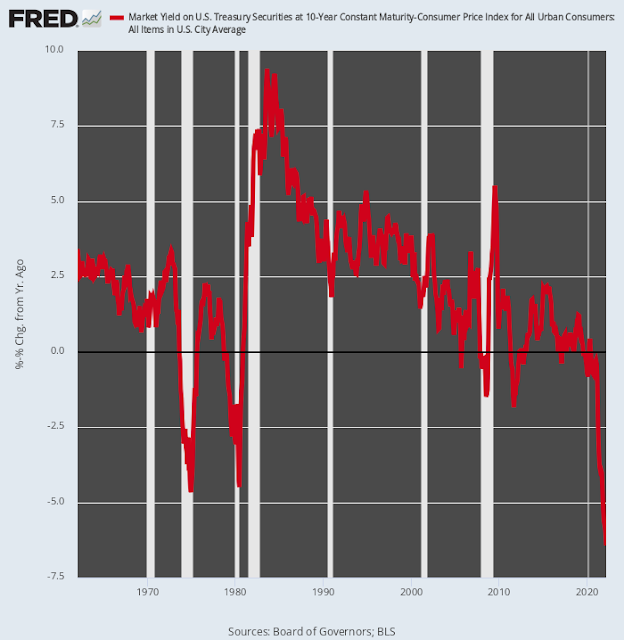

What is the Fed’s remedy for combatting today’s rampant inflation? It raised the Federal Fund Rate by one-quarter of one percent (.25%) at its last meeting. When that was followed by a further surge in inflation, it hinted that it may raise the rate by one-half of one percent (.50%) at its next meeting and perhaps another .50% at its following meeting. With CPI inflation at 9% (and real inflation near 13%), that means by the end of this year the return on ten-year Treasuries will still be negative 7% (11% real). This chart shows the real ten-year yields. “Behind the curve” does not begin the describe the Fed’s pathetic response to this crisis of its own making.

If you believe that the President is an empty suit, Congress is a mob of fiscally challenged morons and the Fed is incompetent at fulfilling its most basic functions, what does that mean? It means that you are on your own. Instead of looking to them to make things better, plan on them continuing to make things worse.

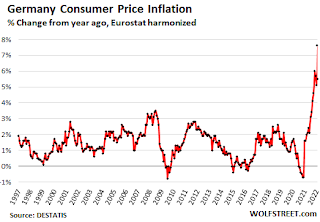

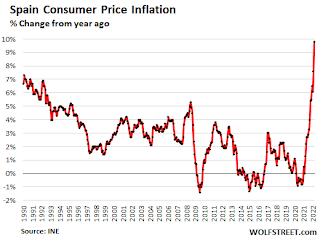

The World’s Economies Suffer Slow Growth and High Inflation

The US is not the only place facing dire problems. In 2021, 45% of EU gas imports came from Russia, up from 26% in 2010. The three largest economies import huge amounts of their gas supplies from Russia: Germany: 55%, Italy: 45%, France: 17%. Russia also accounts for 10% of the world’s oil supply. It exports almost 5 million barrels of crude oil and 2.8 million barrels of refined products every day. Much of that goes to European countries. Finland and Hungary get almost all their oil from Russia. Poland gets more than 55%. Germany and the Netherlands get upward of 40%. As a result, it is no surprise that Germany is resisting the clamor to cease importing Russian oil and gas, the profits of which fund Russia’s brutal “special military operation” in Ukraine.

How did Germany find itself in its untenable energy situation? Following the Three Mile Island accident in 1979 in the US and then the Chernobyl catastrophe in 1986 many Germans became concerned about nuclear power. In the early 2000’s Chancellor Gerhard Schroeder and the big utilities agreed to a nuclear phaseout over 32 years. Angela Merkel, then opposition leader of the CDU party, shrilly opposed it, calling the plan the “destruction of national property.” She asserted that plan would be revoked if her party came to power. In 2011, Merkle was the Chancellor of Germany. Her party was in danger of losing an election in the important state of Baden-Wurttemberg. In an effort to win over some voters from the Green Party, she agreed to press for the closure of Germany’s nuclear power plants. As a result, only three now remain open and all of them are scheduled for closure by the end of this year. In short, to gain a personal political advantage, Merkel agreed to the final closing of Germany’s home grown and cleanest base load electrical supply source. Thus, Germany became dependent on Russian gas to keep its lights on, its homes heated and its factories working.

The EU is facing the same high inflation as the US. It too results from the European Central Bank’s monumental monetary stimulus since 2008. As the pain of rising prices grows, there will be a demand for “price controls” and politicians will likely serve them up to prove that they are “doing something” even if that something quickly leads to far bigger problems.

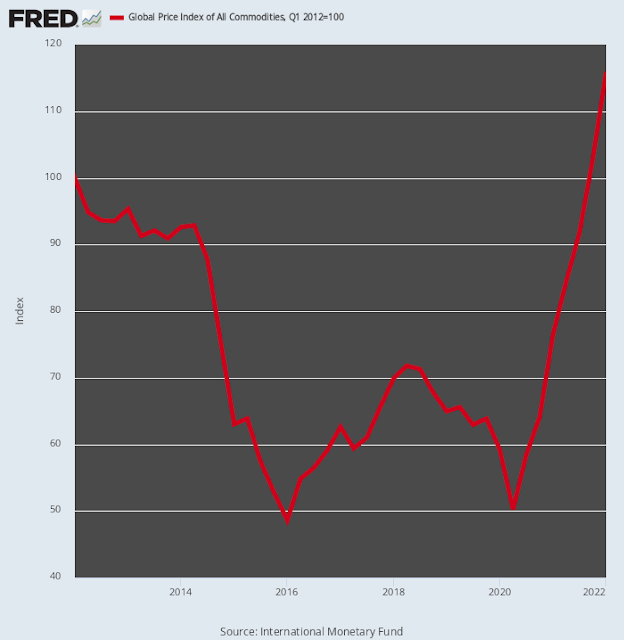

As the ECB dithers over raising rates and rolling off its assets, Fed economists insist that US inflation will soon moderate. However, rising consumer prices are baked into the cake because all commodity costs are rising sharply.

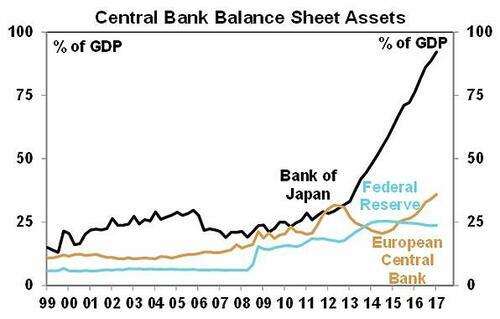

Chinese manufacturing is seriously impacted by that nation’s extreme Covid responses. Shipping container rents are soaring as containers stack up in Chinese ports. The city of Shanghai, population 25 million, is in lock down. The Japanese yen is in near free fall. The Japanese central bank recently asked US Treasury Secretary Janet Yellen for help in arresting the fall. It was politely turned down. The dated chart on the next page reveals the cause of the yen’s problems.

It is estimated that the Bank of Japan (BOJ) holds around ¥35 trillion of Japanese stocks on its balance sheet. That is roughly 80% of Japan’s entire ETF market. It is not an exaggeration to say that the BOJ has engaged in a "stealth nationalization" of Japanese industry.

One thing we can count on is that governments will continue to print money in great excess just as they have done for decades. Ray Dalio explains why,

When one can manufacture money and credit and pass them out to everyone to make them happy, it is very hard to resist the temptation to do so. It is a classic financial move. Throughout history, rulers have run up debts that won’t come due until long after their own reigns are over, leaving it to their successors to pay the bill. When governments print a lot of money and buy a lot of debt, they cheapen both, which essentially taxes those who own it, making it easier for debtors and borrowers. When this happens to the point that the holders of money and debt assets realize what is going on, they seek to sell their debt assets and/or borrow money to get into debt they can pay back with cheap money. They also often move their wealth into better storeholds, such as gold and certain types of stocks, or to another country not having these problems. At such times central banks have typically continued to print money and buy debt directly or indirectly (e.g., by having banks do the buying for them) while outlawing the flow of money into inflation-hedge assets, alternative currencies, and alternative places. Of the roughly 750 currencies that have existed since 1700, only about 20 percent remain, and all of them have been devalued. When the creation of money sufficiently hurts the actual and prospective returns of cash and debt assets, it drives flows out of those assets and into inflation-hedge assets like gold, commodities, inflation-indexed bonds, and other currencies (including digital). This leads to a self-reinforcing decline in the value of money.

It is useful to understand what is known in economics as the “Cantillion Effect.” The first people to get their hands on newly printed money benefit the most. Then prices rise and the vast majority of people pay higher prices. Thus, the rich get richer and the poor get poorer – exactly as has been happening since 2008. This can only happen in a country with a strong central government. Indeed, it always ends up happening with such governments as explained in an article from Mises Wire with quotes from Hayek’s epic work, “The Road to Serfdom.”

Before Western civilization fell prey to the siren calls of big government, there used to be safeguards in place to prevent any temporary ruler from causing too much damage. With a small government, heavily restricted in the domains within which it could operate and with sound money limiting it from venturing too far from its financial obligations, there was only so much harm that even a buffoon could cause. A small government that’s radically constricted in what it may do or opine on isn’t primarily a call for letting ruthless capitalists run free. It’s to protect against the inevitable idiot that will one day run the operations of government: “The problem with (vast) government power is that eventually some distasteful person will turn those powers on you—by which time it’s too late for you to regret ever supporting the expansion of its influence.” An activist government, democratic or not, wishes to improve upon the outcomes of the private sector and civil society. Obstacles like gold standards, constitutions, and government budgets must go. A government constricted cannot do the things its proponents dream of. This is why modern economists—and British economic historians in particular—don’t grasp the events of the 1920s.

MMT (Modern Monetary Theory) "works" in the short term - for the benefit of a small group of politically favored people. This is the “seen” outcome. However, as Henry Hazlitt and Frédéric Bastiat have explained, proper economics require examining the long-term effects of a policy on everyone. This is the “unseen” outcome. Capitalism is the means by which goods and services are efficiently produced from scarce resources; MMT is the means by which they are given to favored groups without regard to the negative impacts on production and prices.

Lenin wrote long ago that, “The surest way to ruin a nation is to debauch its currency.” That should seem obvious to any sentient being. Unfortunately, it is not obvious to anyone working in government. Consequently, government goals inevitably end up being at odds with your goals - as this fifty-year chart of the decline of the dollar shows.

The Fed and government apologists will argue that the US dollar index (DXY) has recently been rising. But this is a clever deception. It compares the dollar to several other currencies including the Pound Sterling, Euro and Yen. They are all sinking ships and the fact that the dollar is currently sinking somewhat slower than the others is not a cause to celebrate. The dollar may presently be the least dirty shirt in the hamper but that does not make it a desirable asset.

1- We regularly include charts published by “FRED.” They are produced by the Federal Reserve Bank of St. Louis. It has a huge number of searchable charts and data. They can be found at fred.stlouisfed.org

2 - Stochastic models purport to statistically analyze “random probability distributions.” It is like claiming the ability to predict the future.

If you find this material interesting feel free to sign up to have it delivered directly to you by going to WorldViewInvesting.com, click on the top left corner icon and select the “Subscribe” button. We will not share your email with anyone. If you are not receiving issues, please check your spam/junk folder and then “whitelist” us.

Important Message: The foregoing is not a recommendation to purchase or sell any security or asset, or to employ any particular investment strategy. Only you, in consultation with your trusted investment advisor, can select the strategy that meets your unique circumstances, investment objectives and risk tolerance.